Payment Plan Agreement Template

A Payment Plan Agreement is a document that shows when and how a borrower will repay a debt. It typically includes the total amount owed, payment schedule, accepted payment methods, and what happens if payments are late or missed.

Fill forms in a few steps

Save, print & download

Done in 5 minutes

What Is an Agreement Letter for Payment?

A Payment Plan Agreement is a legal document used to outline the repayment of a loan. It is a legally binding agreement. There are two parties involved, the lender and the borrower.

The lender can be a:

- Bank

- Individual

- Business A Payment Agreement Letter includes:

- The total amount owed

- When payments are to be made

- Accepted payment methods

It also typically explains what happens if the borrower defaults on payments or pays after the specified dates.

This type of document is especially useful if you’ve borrowed a large sum of money, as it gives both parties a clear repayment structure. This can give the lender peace of mind and help the borrower organize their repayments. A Letter of Agreement for Payment is not as detailed as a Loan Agreement. However, it’s still legally binding and can be enforced in court.

Why Create a Payment Plan Agreement

The importance of an Agreement Letter of Payment lies in the benefits it offers to both borrower and lender. Here are some of the benefits:

| Benefit | What It Means |

|---|---|

| Clear terms | Shows how much is owed, when payments are due, and how to pay. |

| Legal protection | It’s legally binding and can be used in court if the terms aren’t followed. |

| Builds trust | Both sides feel safer because the plan is written down. |

| Prevents disputes | Reduces confusion and helps avoid arguments later. |

| Sets consequences | Explains what happens if a payment is late or missed. |

| Proof for records | Gives you a written record for personal files (and sometimes taxes). |

| Helps with budgeting | A set schedule makes it easier to plan payments and stay on track. |

In short, a Payment Agreement Letter can reduce the risk for the lender and create more trust between both parties.

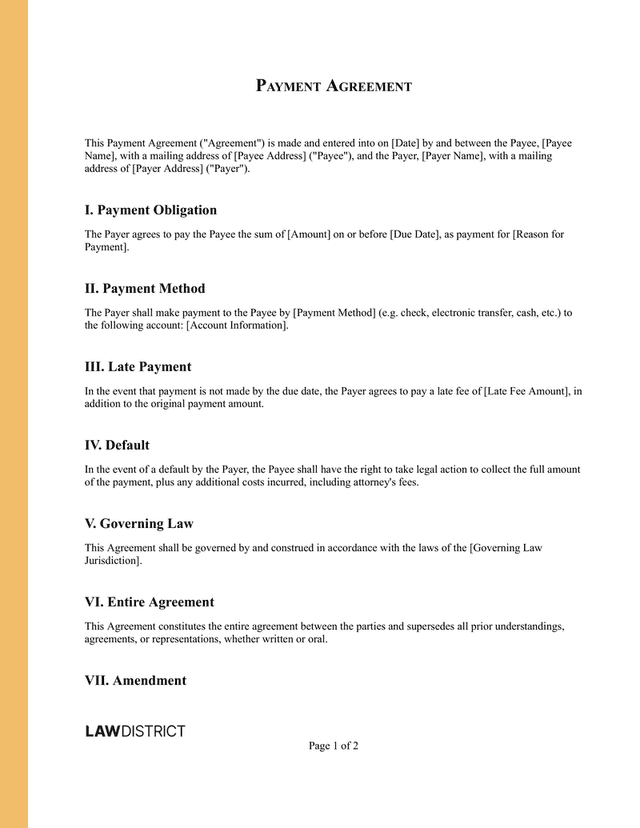

Sample Letter of Payment Agreement

Here is a sample of a finished version of a Payment Plan Agreement, which you can use to help structure and write your own:

How Do I Write a Payment Agreement

You can easily draft a Payment Agreement by including the following details in your document:

- Identify both parties: Name both the borrower and lender, and include their mailing addresses.

- Payment information: Include details like the payment amount, due date, and the purpose of the loan.

- Payment method: Note the preferred payment method. You should also include the account information needed to make the payments.

- Late payment details: State if there are any consequences to late payment. These can discourage any delays.

- Default details: Clearly outline what happens if the borrower defaults on payments.

- Governing laws: State the governing laws in your jurisdiction. This is typically the location of the borrower or lender.

- Entire agreement clause: This clause states that the document contains all agreed-upon terms and conditions. It supersedes any prior agreements.

- Binding effect: The agreement applies to both parties and anyone who legally takes their place (like heirs or assigned representatives).

- Signatures: Both parties must sign the document.

Each loan is different, so your agreement may need different clauses or provisions.

You can easily create your own personalized version of the agreement with our customizable, free Payment Agreement template.

FAQs About Payment Agreements

Still have some doubts about the use of this document? Here are some answers to some of the most common questions regarding Payment Plan Agreements.

Payment Agreement Letters are generally considered to be legally binding by courts. If both parties have signed the agreement and there has been an exchange of consideration (e.g., goods or money,) the agreement is enforceable. If either party doesn’t comply with the agreement, they may face legal consequences. Nevertheless, specific laws vary by jurisdiction. You should check your local laws for the most accurate information regarding your Payment Plan Agreement.

You can draft your own personalized version using our free online Payment Agreement template. Our template is fully customizable, allowing you to enter any details or clauses you want related to the loan.

Simply enter your details and instantly receive the finished document, ready to be sent or printed.

Try Lawdistrict Now

Instant and complete access to our entire library of legal forms

Edit, download and print in PDF from any device

Save time and money on legal document creation