Free Loan Agreement Template

A loan agreement is a legal contract where a lender provides funds to a borrower, who agrees to repay the amount with interest. This document should detail the loan amount, repayment terms, any collateral offered, and conditions for default.

Trusted by 4,859 users.

Protect your loan in minutes. What is the money for?

Fill forms in a few steps

Save, print & download

Done in 5 minutes

What Is a Loan Agreement?

A loan is an agreement between 2 parties in which one individual or business (known as the lender) lends money to the other party (in this case, the borrower) [1].

This sum is then paid back over weeks, months, or years.

The loan amount is usually returned to the lender in regular installments, and very often a percentage of interest is added to the original amount.

A Loan Agreement is used by these parties to create a clear record of the sum of money that is being lent, the terms of repayment, and any interest that is being levied on the amount.

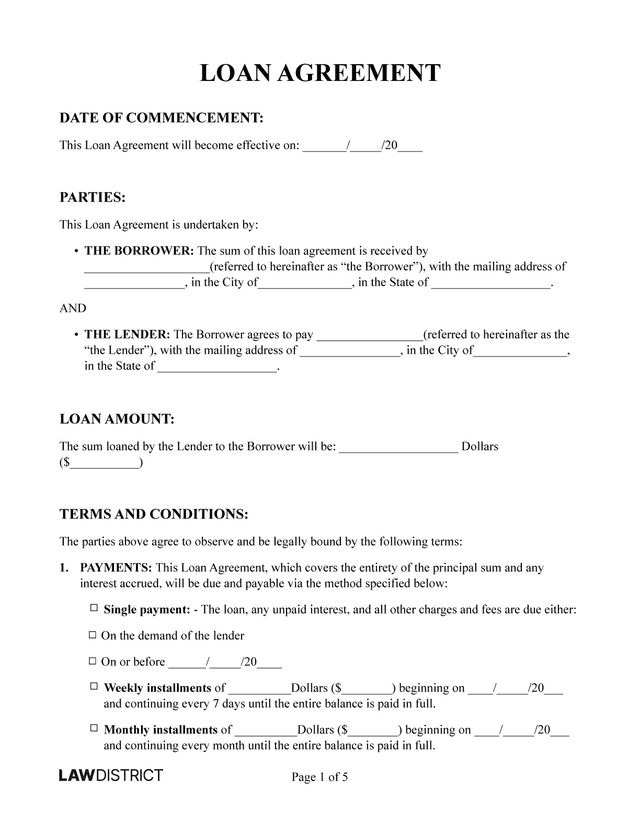

Loan Agreement Sample

Before you start writing and modifying your own Loan Agreement template, it can be helpful to look over a real-life example.

If you’re not sure about the terminology or structure that a completed document should include, simply scroll through our Loan Agreement sample below to get more familiar with the document.

Types of Loan Agreement

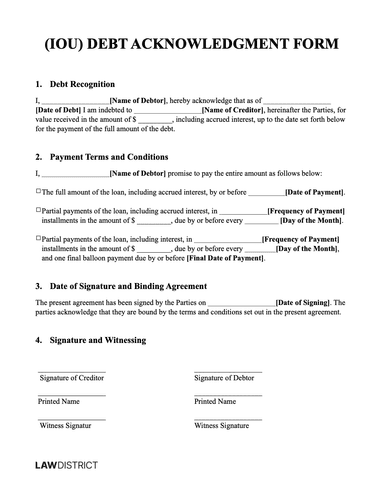

An IOU is an agreement made between a borrower and lender, also known as a friendly loan agreement because it is informal, but it can be used in court

A personal loan agreement allows a borrower and a lender, such as a bank, credit union or online lender, to outline the details of the money being lent

Who Needs a Loan Agreement?

Anyone lending money should use a Loan Agreement. It’s legally enforceable, providing a clear record of the loan terms and protecting both parties in case of disputes.

For borrowers, a Loan Agreement specifies the repayment schedule and interest rates, ensuring transparency and protection against predatory practices and unexpected changes.

How To Write a Loan Agreement

There are a few important points to remember when you write a Loan Agreement.

First, you must use clear and easy-to-understand language so that it is immediately obvious who is who in the agreement and how the money should be repaid.

After all, a Loan Agreement is a legally enforceable contract, so it must be obvious to anyone reading it what the terms are and who the parties bound by it are [2].

There should be no ambiguity at any stage, or it could lack the clout necessary to hold a breaching party to account.

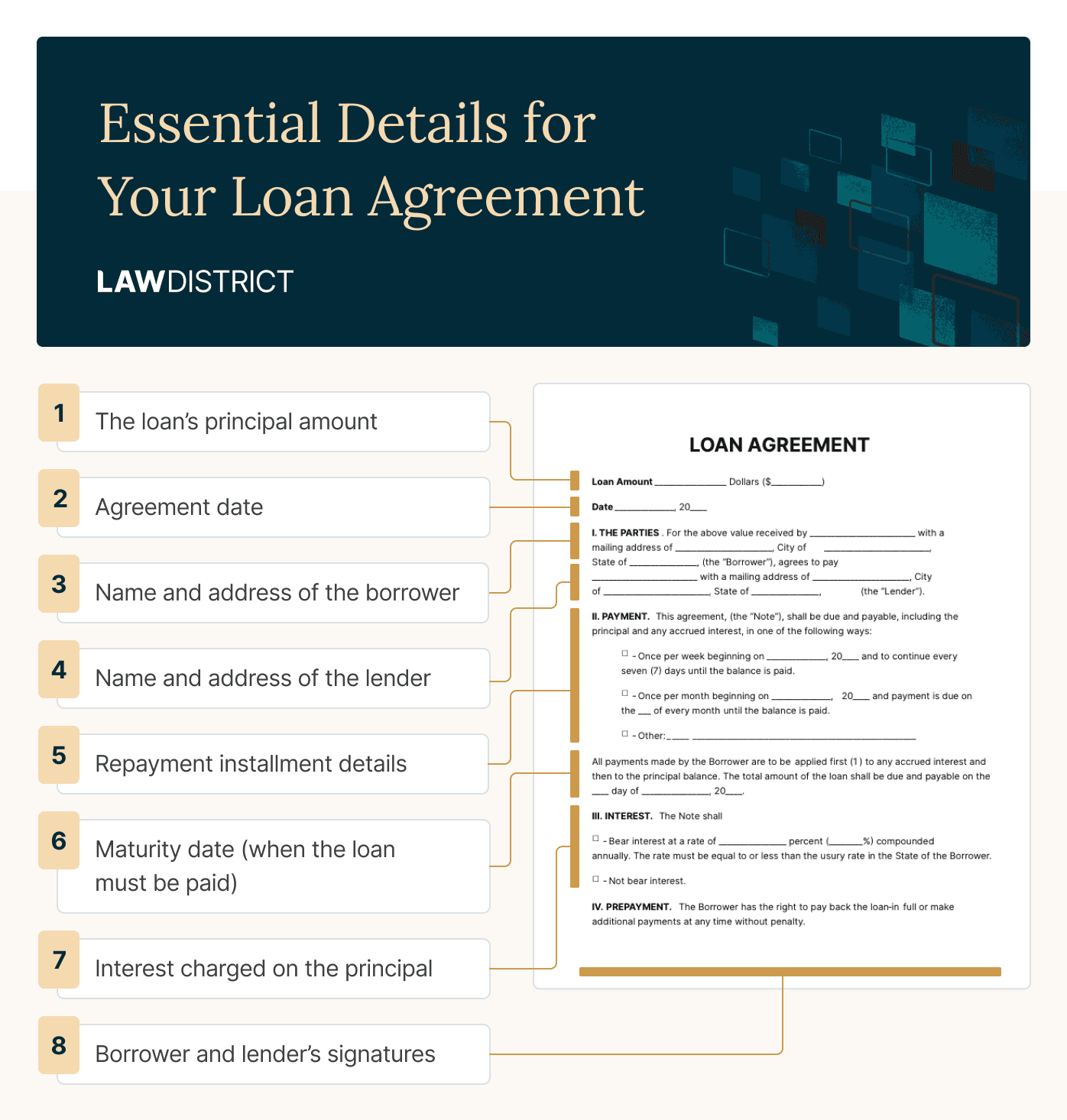

To correctly include these elements in your Loan Agreement, you must include the following loan details:

- Date of commencement: Include when the Loan Agreement will begin

- Parties: Enter the full names and complete addresses of both the Borrower and the Lender. It may also include Social Security and driver’s license numbers for identity verification.

- Loan Amount: Include the amount of money the lender will loan to the Borrower.

- Terms and Conditions: Add how the loan will be paid back (single payment, installments), acceptable payment forms (cash, money order, credit card, wire transfer, etc.), interest, collateral, origination fee, grace period, late fees, prepayment penalty fees, if any, amortization schedules, governing law, etc.

- Signatures: Sign the Loan Agreement with the other party, along with your name and date.

Use our Loan Agreement template as a helpful base to follow these steps better and create your document.

What Should I Include in a Loan Agreement?

Certain basic details must appear in your Loan Agreement no matter what. Failure to include crucial information could lead to your final form proving ineffective when it’s needed most.

The key contractual terms to remember in your Loan Agreement include the following:

- How much is being borrowed (sometimes referred to as the principal sum)

- If it is an unsecured loan or secured loan (a secured loan has a valuable item used as collateral to offset loan risk)

- When the money is being loaned and when it should be paid back

- The amount of interest that is to be charged

- If any late fees or pre payment penalties apply

- What should happen in the event of default by the borrower defaults on the amount

When you complete a Loan Agreement with our specialized advice, you will be prompted to provide these details.

Once complete, you can have your document reviewed by a legal professional to ensure it is ready.

How To Pay A Loan Agreement

Once a Loan Agreement has been finalized and the borrower has received the funds requested, they must follow the repayment schedule specified by the formal contract.

A borrower will often need to repay the loan in installments, usually paying either:

- Monthly payments

- Weekly payments

However, this is not the only possibility open to lenders and borrowers.

If the loan proceeds are smaller, the agreement might stipulate that the outstanding balance has to be paid in a single lump sum on a certain date or when the issuer requests the money back.

Additionally, some agreements will insist that some of the initial loan capital has to be returned via installments with a larger final payment made at the end of the contract (balloon payment).

This normally involves the interest being paid off via installments and the principal balance amount being paid back in full at the end [3].

How To Sign a Loan Agreement

To sign your Loan Agreement, you should check with your jurisdiction to determine if there are any special requirements to fulfill before adding your signature.

In most cases, you are not legally obligated for the signing of the agreement to be witnessed, however, you may wish to sign the document in front of a:

- Notary public

- Witness

Loan Agreement FAQs

There are a lot of details about Loan Agreements that are essential to understand.

Find out what other key details you might need to consider before entering into a lending contract in our FAQs.

Use a Loan Agreement when lending money for real estate, businesses, student loans, or personal purchases. It ensures the borrower honors the deal and provides legal protection.

Always create and sign the agreement before transferring any funds.

A Loan Agreement and Promissory Note are often compared or even mentioned interchangeably.

While they are similar in certain aspects, the legal documents have some key differences.

Check the table below to understand the similarities and differences between the two documents.

| Loan Agreement | Promissory Note |

|---|---|

| There is a promise to repay | There is a promise to repay |

| Includes steps for repayment | Includes steps for repayment |

| There is a repayment timeline | There is a repayment timeline |

| Is legally binding | It is legally binding |

| Includes the signature of the borrower | Includes the signature of the borrower |

| Includes the lender’s signature | Does not include the lender’s signature |

| Can repay in installments | Cannot repay in installments |

| Includes consequences of not paying | Does not include consequences |

A Loan Agreement provides clarity and security, helping avoid disputes and defaults.

If a borrower makes late payments, decides not to pay or the lender changes the repayment terms suddenly, and there is no Loan Agreement, there is little either party can do to enforce the original accord. This could leave one side significantly out of pocket.

Anyone lending money should use a Loan Agreement. It is legally enforceable, providing a clear record of the loan terms and protecting both parties in case of disputes.

For borrowers, a Loan Agreement specifies the repayment schedule and interest rates, ensuring transparency and protection against predatory practices and unexpected changes.

Try Lawdistrict Now

Instant and complete access to our entire library of legal forms

Edit, download and print in PDF from any device

Save time and money on legal document creation