Promissory Note Template

A Promissory Note documents a loan between two or more parties. It sets out the loan's key terms, including repayment terms, the interest rate, and more. Promissory Notes provide a clear record of debt that helps safeguard the borrower and lender in the transaction.

Trusted by 3,034 users.

Fill forms in a few steps

Save, print & download

Done in 5 minutes

What Is a Promissory Note?

A Promissory Note is a payable document through which a borrower commits to repaying a lender.

While Promissory Notes share many traits with loan agreements, they typically bind only the borrower and are generally less formal. They operate much like IOUs, laying out what one party owes another.

Even so, these documents carry more substantial legal weight than IOUs, and are more readily enforceable, which offers significantly better protection for lenders.

What Is a Promissory Note in Real Estate?

A promissory note in real estate is a written promise by the buyer (borrower) to repay a specific amount of money to the lender under agreed terms.

It sits behind the property loan and clearly sets out the principal, interest rate, repayment schedule, and what happens if payments are missed.

In many cases, it's used together with a mortgage or deed of trust, which secures the loan against the property if the borrower defaults.

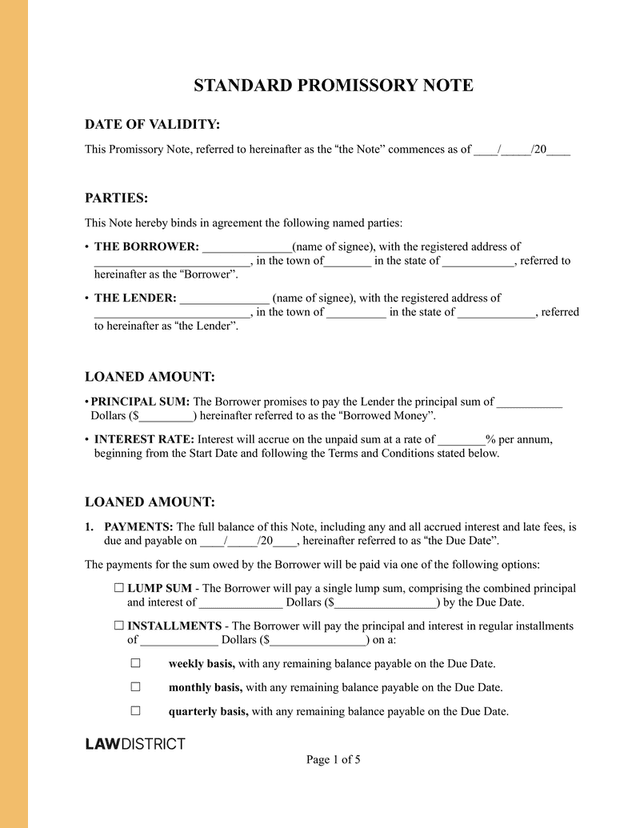

Promissory Note Sample

When writing a Promissory Note for the first time, it can help to see a real example first. This will assist you in getting a feel for the structure and terminology of a legally binding document.

Review our Promissory Note example document below to get a better idea of how your final form should turn out.

Importance of a Promissory Note

Promissory Notes are mostly employed for small personal loans or financial agreements between close family and friends.

The following are additional circumstances to help you understand when to use a Promissory Note:

- Real estate loans: For a private mortgage when buying a home.

- Debt loans: Informal loans between friends or family to avoid disputes.

- Business loans: Borrowed from banks, with liens placed on assets until paid.

- Student loans: Loans for education, also called master Promissory Notes.

- Vehicle loans: Lists payments required to fully own a car, including vehicle details.

- Other loans: For example, corporate investments where non-payment may transfer ownership to the lender.

What To Do if the Borrower Defaults

If the borrower misses a payment, first review your Promissory Note to confirm the due dates, grace period (if any), and late-payment or default clauses.

Once you've done that, contact the borrower in writing to remind them of the missed payment and to request immediate payment or the creation of a repayment plan.

Creating a formal demand letter is often the first step before taking further action.

If the borrower still does not pay, you may enforce your rights under the note. For a secured note, this may include repossessing or selling the collateral in accordance with local law.

For an unsecured note, you may need to file a claim in small claims or civil court to obtain a judgment and pursue collection. Throughout the process, remember to keep copies of all communications and payments.

Types of Promissory Notes

Different types of Promissory Notes exist. Depending on your situation, one kind may be more suitable than the other.

There are 2 basic types of Promissory Notes:

- Secured Promissory Note: This type of Promissory Note is used to secure collateral, for example, a vehicle or television. If the borrower does not make timely repayment of the secured loan, the lender has the right to claim the property.

- Unsecured Promissory Note: This is a loan without collateral, which is more common for smaller personal loans between friends or family members. If the borrower fails to repay, the lender must rely on collection efforts or file a claim in court to enforce the debt.

With our Payment Agreement template, you can create the type of note that best suits your needs.

How To Write a Promissory Note

To prepare a Promissory Note, include all the key details of the loan in clear, simple language. Use the steps below as a checklist when drafting your document.

- State the loan purpose: Specify why the loan is being made, such as business, real estate, vehicle, education, bills, or another reason.

- Identify the lender: Indicate whether the lender is an individual or a company, and record their full legal name and address.

- Identify the borrower: Mention if the borrower is an individual or company, and include their full legal name and address, and list any additional borrowers.

- Record the loan amount and date: Write the total amount that is being lent and the date on which the money will be repaid.

- Set the interest and payment terms: Decide whether interest will be charged, including the rate if applicable, and choose whether repayment is in a lump sum, by regular payments, by a fixed date, or on demand.

- Add collateral, late payment, and extra clauses: State whether any property secures the loan. Also, describe late payment penalties if used, and include any additional terms you want to apply.

- Sign the document: Sign and date the Promissory Note with the other party (and any co-borrowers), and have witnesses or a notary public present if required.

Use our Promissory Note legal template as a smart legal solution to help you draft your essential details to make your loan official.

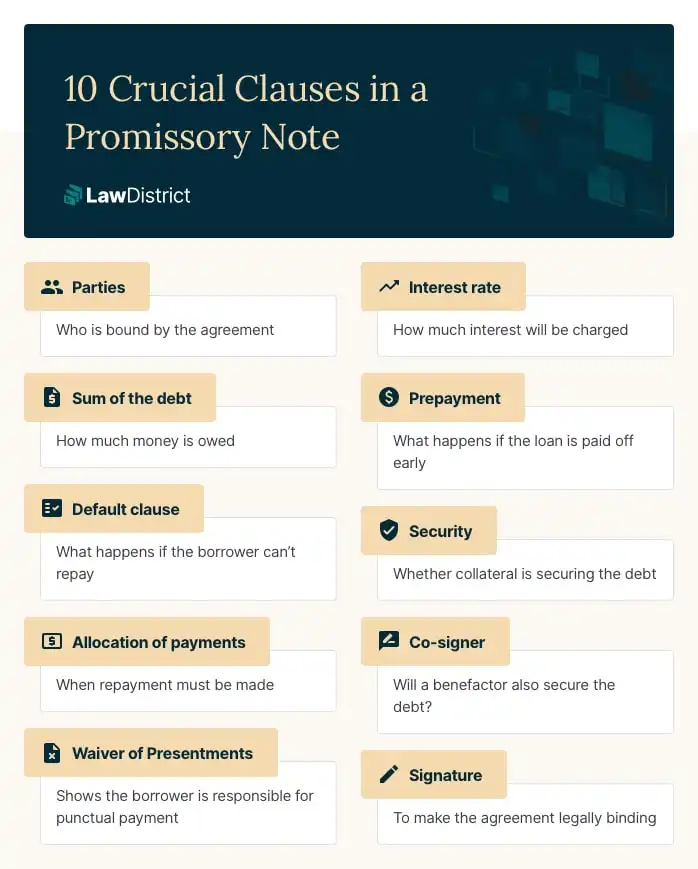

Key Promissory Note Clauses

When drafting your Promissory Note, it's important to include certain clauses. Below are the key clauses that are typically found on the document:

Do I Need Witnesses To Sign the Promissory Note?

There is no obligation for the signing of your Promissory Note to be witnessed, but it can be a lender requirement in some cases.

Witnessing adds more legitimacy to the signing of your debt note. It ensures all parties are fully aware of the contract terms and that they agree to them.

Does a Promissory Note Need To Be Notarized?

Promissory Notes typically do not require notarized signatures, so you do not need to sign the document in front of a notary.

However, you and the borrower can still choose to get the document notarized to add an extra layer of security and certainty to the signed document and maximize enforceability.

Usury Laws by State

If you have decided to charge interest on the loan amount, ensure you adhere to state laws and regulations.

Refer to our table below to confirm the maximum interest rate in your state:

| State | Law | Maximum Interest Rate |

|---|---|---|

| Alabama | § 8-8-1 | 8% for contracts in writing, 6% for verbal agreements |

| Alaska | § 45.45.010 | 5% above the 12th Federal Reserve District Interest rate on day loan was created, or 10%, whichever is larger (loans less than $25,000). No maximum interest rate exists for amounts over $25,000 |

| Arizona | § 44-1201 | No limit exists for loans in writing 10% per annum for any loans not in writing |

| Arkansas | § 4-57-104 | Cannot exceed the 17% maximum established in the Arkansas Constitution (Amendment 89) |

| California | § Article XV | 10% for personal, family, and household loans. The highest of 10% or 5% over the amount charged by the Federal Reserve Bank of San Francisco |

| Colorado | § 5-12-103 & § 5-2-201 | 45% maximum interest rate for supervised loans 12% maximum interest rate for unsupervised loans |

| Connecticut | § 37-4 | The limit is 12% |

| Delaware | § tit. 6,2301 | 5% limit over the Federal Reserve Discount rate at the time the loan was created |

| Florida | § 687.03 | 18% on loans below $500,000 25% on loans over $500,000 |

| Georgia | § 7-4-2 | 5% per month on amounts over $3,000 7% without a written contract 16% on loans under $3,000 |

| Hawaii | § 478-2, § 478-3, & § 478-4 | 10% limit without a written contract 12% is the general maximum interest rate 10% is the maximum on judgments |

| Idaho | § 28-22-104 | The general maximum rate is 12% The maximum rate on court judgments is 5% |

| Illinois | § 815 ILCS 205/4 | 9% general usury limit |

| Indiana | § 24-4.6-1-102 & § 24-4.5-3-201 | 8% is the maximum without an agreement 25% for consumer loans that are not supervised |

| Iowa | § 535.2(3)(a) | The general maximum interest rate is 5% If the interest |

| Kansas | § 16-201 & §16-207 | 10% legal interest rate 15% general maximum interest |

| Kentucky | § 360.010 | 8% legal rate of interest The maximum interest rate is 4% larger than the Federal Reserve rate (or 19%, whichever is less) There is no limit when stated in a written contract with a loan larger than $15,000 |

| Louisiana | § 9:3500 | 12% general maximum interest rate |

| Maine | § tit. 9-B, § 432 | 6% legal interest rate (no maximum in any statute) |

| Maryland | § 12-102 103 | 6% legal interest rate 8% maximum interest rate with a written contract |

| Massachusetts | § 3 & Ch. 271, § 49 | 6% legal interest rate without a written contract Normally does not go over 20% (if part of the contract) |

| Michigan | § 438.31 | 5% legal rate 7% with a written contract |

| Minnesota | § 334.01 | 6% legal rate of interest 8% maximum interest rate for written contracts No limit if the amount is over $100,000 |

| Mississippi | § 75-17-1 | 8% legal rate of interest The rate may be increased up to 5% or 10% above the Federal Reserve discount with a contract |

| Montana | § 31-1-107 | The highest of 15% or 6% over the Federal Reserve System rate |

| Nebraska | § 45-101.03 | 16% maximum usury rate |

| Nevada | § 99.050 | The least of 36% or the maximum rate allowed under the Military Lending Act |

| New Hampshire | § 336:1, § 358-A:2 | No legal limit exists for interest rates |

| New Jersey | § 31:1-1 | 6% without a written contract 16% with a written contract |

| New Mexico | § 56-8-3 | 15% maximum without a written contract |

| New York | § 5-501 & § 14-A | 6% legal interest rate 16% general usury limit |

| North Carolina | § 24-1 | 8% legal rate Consumers and creditors are allowed a higher contractual rate |

| North Dakota | § 47-14-09 | 5.5% maximum interest rate above the current maturity rate of Treasury bills for six months prior to the issuance of the loan for written contracts less than $35,000, or 7%, whichever amount is greater |

| Ohio | § 1343.01 | 8% interest rate in any written contract |

| Oklahoma | §266 | 6% legal rate of interest without any contract |

| Oregon | § 82.010 | 9% legal interest rate 15% or 5% greater than the 90-day discount rate of commercial paper for business and agricultural loans |

| Pennsylvania | § 201 | 6% interest rate |

| Rhode Island | § 6-26-2 | 21% or domestic prime rate plus 9% maximum interest rate |

| South Carolina | § 37-3-201 | 10% maximum interest rate unless stated otherwise in a contract |

| South Dakota | § 54-3-4 & § 54-3-16(3) | No limit exists for written agreements 12% maximum interest rate without a written agreement |

| Tennessee | § 47-14-103 | 10% maximum interest rate unless stated otherwise in a contract |

| Texas | § 302.001(b) | 10% interest rate Can be higher if the loan is provided by contract law |

| Utah | § 15-1-1 | 10% maximum interest rate unless stated otherwise in a contract |

| Vermont | § 41a | 12% rate of interest unless it falls under a particular circumstance provided in § 41a |

| Virginia | § 6.2-301 & § 6.2-303 | 6% legal rate 12% with a contract |

| Washington | § 19.52.020 | 12% maximum interest rate, or 4% over the average bill rate for 26-week treasury bills in the month the loan took effect |

| Washington D.C. | § Title 29, Chapter 33 | 24% maximum interest rate for written contracts 6% maximum interest rate for verbal contracts |

| West Virginia | § 47-6-5 | 6% legal interest rate 8% maximum interest rate for written agreements |

| Wisconsin | § 138.04 | 5% legal interest rate Interest rates in written agreements can be agreed upon |

| Wyoming | § 40-14-106 | 7% interest rate Interest rates in written agreements can be agreed upon |

Calculate Loan Interest Rate

Similar to loan agreements, loans secured through a Promissory Note can demand a fair interest rate on the principal amount.

Interest protects against borrower payment default, especially if the loan is not secured against any collateral and spreads over a long period. A minimum interest rate, known as the federal reserve rate [3], should be charged to avoid the Internal Revenue Service classifying the loan as a gift.

When using debt instruments that levy interest, it’s important to remember that state usury laws apply. Take this into account when drafting your Promissory Note.

Other Financial Documents

A Promissory Note can be helpful in many situations. If your circumstances change, you may find these other documents related to loans helpful:

Promissory Note FAQs

It is crucial to be fully clear on what your Promissory Note should contain before creating your document. If you are still unsure of the details, read through our FAQs below to learn more about their purpose and essential elements.

Like most signed formal agreements and contracts, Promissory Notes must follow state and federal financial and legal regulations. Otherwise, they may be declared invalid.

Breaching usury laws, losing all copies of the note, including false or incorrect information, and being unable to prove legal ownership of the debt could nullify your agreement.

Both a Promissory Note and a loan agreement have key similarities and differences, and understanding both will help you decide which one is best for you.

A Promissory Note is a simpler document where the borrower makes a clear, written promise to repay a specific amount under set terms.

A Loan Agreement is more detailed and often used for larger or more complex loans. It can include extra provisions such as representations, covenants, conditions, and detailed remedies. In practice, promissory notes are used for straightforward loans, while loan agreements govern broader lending relationships.

To release a Promissory Note, verify that the borrower has paid the debt or that you have forgiven it. You must then complete and sign a Promissory Note release form that lists the parties, dates, and amount. Once you have that, give the signed document to the borrower and keep a copy.

Similar to loan agreements, loans secured through a Promissory Note can demand a fair interest rate on the principal amount.

Interest protects against borrower payment default, especially if the loan is unsecured and spreads over a long period. A minimum interest rate, known as the Federal Reserve rate [[3]], should be charged to avoid the Internal Revenue Service classifying the loan as a gift.

When using debt instruments that levy interest, it's important to remember that state usury laws apply. Take this into account when drafting your Promissory Note.

Try Lawdistrict Now

Instant and complete access to our entire library of legal forms

Edit, download and print in PDF from any device

Save time and money on legal document creation