Key Takeaways:

- Usury laws set limits on interest rates lenders can charge, protecting borrowers from excessive costs.

- Exemptions allow certain lenders, like banks and credit unions, to bypass these caps under state and federal rules.

- **States vary widely in maximum rates, from strict caps like Iowa's 4% to flexible rates like Colorado's 45% for installment loans.

- Loans covered include mortgages, personal loans, credit cards, and even some security deposits.

- Penalties for violations include rate adjustments, fines, license revocation, and legal consequences.

While many Americans are affected by substantial debt, very few pay attention to the interest rates lenders charge, falling victim to usury. Usury laws are put in place to protect consumers from being overcharged when they borrow money.

Most states have set a legal limit to the amount lenders can charge for various loans. For example, in California, the maximum legal amount a lender can charge for goods or money for family, household, or personal use is 10%.

However, many lenders, such as banks, savings and loans, credit unions, and finance corporations, are exempt from this limit due to federal preemption and state exemptions, allowing them to charge higher rates.

Some charges with interest are may also be exempt from usury laws. These may include payday loans from licensed lenders, real estate loans secured by property liens, loans from pawnbrokers, and late fees.

As a consumer, it is important to understand the rules and exemptions regarding borrowing money to safeguard yourself from being exploited by lenders. This article will give you reliable information on usury law regulations, how they affect your loan, and the penalties a lender receives when violating these guidelines.

What Are Usury Laws?

Usury refers to the act of imposing excessively high or unfair interest rates on borrowed money.

Usury laws are the rules and regulations governing the interest lenders can charge on every loan a consumer takes. Usury laws target lenders who want to enrich themselves by setting excessively high lending rates. These guidelines set a cap on the highest rate of interest you can be charged for specific loans.

In the United States, every state has its own usury laws supported at the federal level under the Preemption of State Usury Laws (Title 12, Chapter I, Part 190). Examples of loans affected by usury laws include:

- Mortgages

- Credit cards

- Payday loans

- Personal loans It is important to remember that usury laws do not only cover loaned money. They also apply to any capital with interest charged against the principal, like security deposits in lease agreements or mortgages.

Usury laws help you know which loans are safe to take, the institution addressed under these laws, and the maximum rate of interest set in your state. This knowledge will help you better manage and settle your debts.

Usury Laws By State

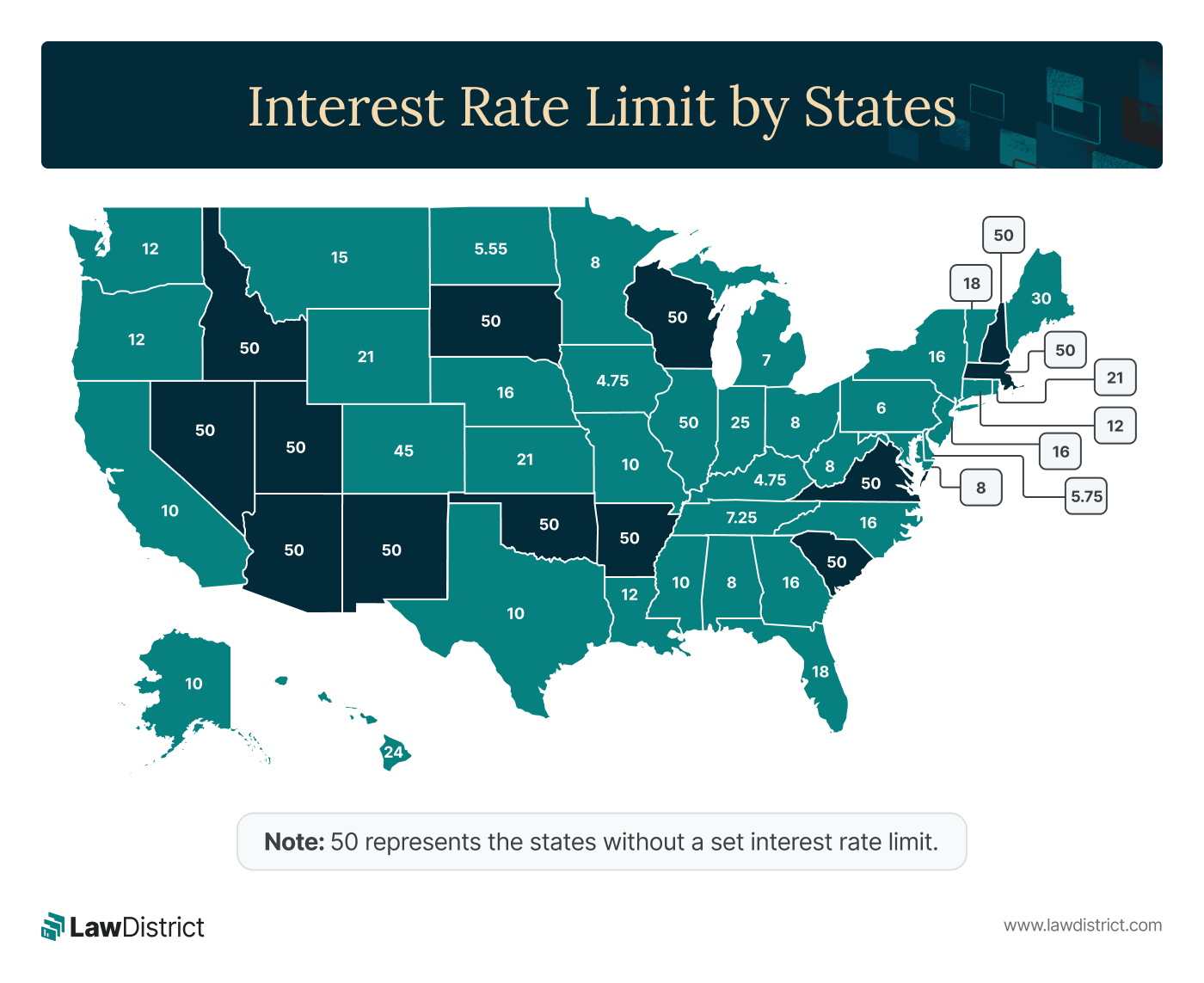

Each state has its own guidelines on the interest rate charged and exemptions allowed. Some states have rigorous usury limits, while others offer lenders some leniency in their regulations. For example, Iowa sets its rate of interest limit at 4% while Colorado sets it at 45% for an installment loan of $2,000 issued by a bank. The following map shows all 50 states' interest rate limits for the same loan amount.

What Is the Maximum Rate Under Usury Law?

The maximum rate under usury law is the highest interest amount and fees a lender can charge on a loan. Some states have strict measures on the maximum rate charged, but other states are more flexible. The maximum rate in these states is determined by:

- The loan type and size

- The entity or person taking the loan

- Both parties agree on the limit

- Contract signed

An example of a state with a flexible maximum rate is Virginia. In the Code of Virginia, the maximum rate is 12% for a loan with a written agreement. However, state banks and savings institutions are exempt from this rate and can charge any interest rate, but the borrower has to agree (Code of Virginia § 6.2-303).

Usury Laws and Loans

Usury laws have a direct impact on the loans consumers take by limiting the amount lenders can receive as profit from the issued loan.

These guidelines protect borrowers from exploitative and unfair interest rates while allowing lenders to receive reasonable revenue. Personal loans primarily benefit from these regulations across all states, while other loans vary depending on the state the consumer resides in and the loan agreement entered.

Who Is Exempt From Usury Laws?

Exemption from usury laws differs depending on the state's regulation in place and legal framework. The following are examples of entities that may be exempt from usury laws:

- Member-owned credit unions with a unique structure and regulatory framework.

- Some banks and financial institutions have a special role in the financial system.

- Government loans, such as federal student loans, may have a different interest rate regulation outside the standard usury laws.

- Commercial loans between large corporations.

- Licensed pawn shops may be exempt due to their collateral-based nature.

- Non-profit organizations taking loans for charitable purposes.

A major example of this exemption is that lenders incorporated out-of-state may charge up to their home state's maximum interest rate—a benefit often utilized by credit card companies with national customer bases and federally chartered banks. (12 U.S. Code § 85)

For this reason, many financial organizations choose to incorporate in states like South Dakota or Delaware.

Even though these entities are exempt from usury laws, it doesn't mean they can charge excessively high interest rates. If the lender is found to have gone overboard, you can receive the interest you paid above the legal limit set—under the state's usury exemption laws.

Penalties for Usury Law Violations

Violation penalties for usury laws vary depending on how severe the violation was, the jurisdiction in which the violation occurred, and the specific guidelines in place.

All states take usury law violations seriously to protect consumers and prevent the vice from progressing. Once a lender is found guilty of violating any usury law, the following penalties can be enforced:

- Adjust the interest rate to comply with the legal limit, and the consumers receive what was overpaid.

- Receive a fine for each violation ranging from $2,500 to $5,000 in various states.

- Criminal charges for severe violations (leading to fines, probation, and imprisonment)

- License revocation on rare occasions where the violations affected numerous people for an extended period.

- Class action (leading to significant financial liability to the institution).

Even with these penalties in place, lenders can take advantage of your situation and use documents with hidden clauses. Before signing a credit card or loan agreement, ensure you use a document that includes the interest rate and fees charged.

It’s crucial to know that committing usury can seriously damage the validity of your legal contracts. This won’t only lead to the legal consequences mentioned above but could also cause documents securing your loans to be voided, making it harder to collect outstanding debts you are owed.

Helpful Resources:

eCFR 12 CFR Part 190 - Preemption of State Usury Laws

WalletHub - Usury Laws by State, Interest Rate Caps

Washington State Department of Financial Institutions - Usury Law

Key Takeaways:

- Usury laws set limits on interest rates lenders can charge, protecting borrowers from excessive costs.

- Exemptions allow certain lenders, like banks and credit unions, to bypass these caps under state and federal rules.

- **States vary widely in maximum rates, from strict caps like Iowa's 4% to flexible rates like Colorado's 45% for installment loans.

- Loans covered include mortgages, personal loans, credit cards, and even some security deposits.

- Penalties for violations include rate adjustments, fines, license revocation, and legal consequences.

While many Americans are affected by substantial debt, very few pay attention to the interest rates lenders charge, falling victim to usury. Usury laws are put in place to protect consumers from being overcharged when they borrow money.

Most states have set a legal limit to the amount lenders can charge for various loans. For example, in California, the maximum legal amount a lender can charge for goods or money for family, household, or personal use is 10%.

However, many lenders, such as banks, savings and loans, credit unions, and finance corporations, are exempt from this limit due to federal preemption and state exemptions, allowing them to charge higher rates.

Some charges with interest are may also be exempt from usury laws. These may include payday loans from licensed lenders, real estate loans secured by property liens, loans from pawnbrokers, and late fees.

As a consumer, it is important to understand the rules and exemptions regarding borrowing money to safeguard yourself from being exploited by lenders. This article will give you reliable information on usury law regulations, how they affect your loan, and the penalties a lender receives when violating these guidelines.

What Are Usury Laws?

Usury refers to the act of imposing excessively high or unfair interest rates on borrowed money.

Usury laws are the rules and regulations governing the interest lenders can charge on every loan a consumer takes. Usury laws target lenders who want to enrich themselves by setting excessively high lending rates. These guidelines set a cap on the highest rate of interest you can be charged for specific loans.

In the United States, every state has its own usury laws supported at the federal level under the Preemption of State Usury Laws (Title 12, Chapter I, Part 190). Examples of loans affected by usury laws include:

- Mortgages

- Credit cards

- Payday loans

- Personal loans It is important to remember that usury laws do not only cover loaned money. They also apply to any capital with interest charged against the principal, like security deposits in lease agreements or mortgages.

Usury laws help you know which loans are safe to take, the institution addressed under these laws, and the maximum rate of interest set in your state. This knowledge will help you better manage and settle your debts.

Usury Laws By State

Each state has its own guidelines on the interest rate charged and exemptions allowed. Some states have rigorous usury limits, while others offer lenders some leniency in their regulations. For example, Iowa sets its rate of interest limit at 4% while Colorado sets it at 45% for an installment loan of $2,000 issued by a bank. The following map shows all 50 states' interest rate limits for the same loan amount.

What Is the Maximum Rate Under Usury Law?

The maximum rate under usury law is the highest interest amount and fees a lender can charge on a loan. Some states have strict measures on the maximum rate charged, but other states are more flexible. The maximum rate in these states is determined by:

- The loan type and size

- The entity or person taking the loan

- Both parties agree on the limit

- Contract signed

An example of a state with a flexible maximum rate is Virginia. In the Code of Virginia, the maximum rate is 12% for a loan with a written agreement. However, state banks and savings institutions are exempt from this rate and can charge any interest rate, but the borrower has to agree (Code of Virginia § 6.2-303).

Usury Laws and Loans

Usury laws have a direct impact on the loans consumers take by limiting the amount lenders can receive as profit from the issued loan.

These guidelines protect borrowers from exploitative and unfair interest rates while allowing lenders to receive reasonable revenue. Personal loans primarily benefit from these regulations across all states, while other loans vary depending on the state the consumer resides in and the loan agreement entered.

Who Is Exempt From Usury Laws?

Exemption from usury laws differs depending on the state's regulation in place and legal framework. The following are examples of entities that may be exempt from usury laws:

- Member-owned credit unions with a unique structure and regulatory framework.

- Some banks and financial institutions have a special role in the financial system.

- Government loans, such as federal student loans, may have a different interest rate regulation outside the standard usury laws.

- Commercial loans between large corporations.

- Licensed pawn shops may be exempt due to their collateral-based nature.

- Non-profit organizations taking loans for charitable purposes.

A major example of this exemption is that lenders incorporated out-of-state may charge up to their home state's maximum interest rate—a benefit often utilized by credit card companies with national customer bases and federally chartered banks. (12 U.S. Code § 85)

For this reason, many financial organizations choose to incorporate in states like South Dakota or Delaware.

Even though these entities are exempt from usury laws, it doesn't mean they can charge excessively high interest rates. If the lender is found to have gone overboard, you can receive the interest you paid above the legal limit set—under the state's usury exemption laws.

Penalties for Usury Law Violations

Violation penalties for usury laws vary depending on how severe the violation was, the jurisdiction in which the violation occurred, and the specific guidelines in place.

All states take usury law violations seriously to protect consumers and prevent the vice from progressing. Once a lender is found guilty of violating any usury law, the following penalties can be enforced:

- Adjust the interest rate to comply with the legal limit, and the consumers receive what was overpaid.

- Receive a fine for each violation ranging from $2,500 to $5,000 in various states.

- Criminal charges for severe violations (leading to fines, probation, and imprisonment)

- License revocation on rare occasions where the violations affected numerous people for an extended period.

- Class action (leading to significant financial liability to the institution).

Even with these penalties in place, lenders can take advantage of your situation and use documents with hidden clauses. Before signing a credit card or loan agreement, ensure you use a document that includes the interest rate and fees charged.

It’s crucial to know that committing usury can seriously damage the validity of your legal contracts. This won’t only lead to the legal consequences mentioned above but could also cause documents securing your loans to be voided, making it harder to collect outstanding debts you are owed.

Helpful Resources:

eCFR 12 CFR Part 190 - Preemption of State Usury Laws

WalletHub - Usury Laws by State, Interest Rate Caps

Washington State Department of Financial Institutions - Usury Law

Most Popular Posts

Some states require a motor vehicle bill of sale form; others do not. Even if only for your personal records, anyone who buys or sells a vehicle needs

If you plan to travel with a minor, whether or not you are their parent, you can minimize inconveniences by carrying a few necessary documents...