Key Takeaways

- Land contracts offer flexible financing for buyers with poor credit but come with higher risks, such as balloon payments and less protection.

- Mortgages provide stability with predictable terms but require good credit and a down payment, and they may include costs like PMI.

- Key differences include ownership transfer (immediate with mortgages, delayed in land contracts) and regulatory oversight.

- Choosing the right option depends on credit, finances, and long-term goals.

Many similarities exist between a land contract and a mortgage. Both require monthly principal and interest payments, as well as a down payment. There are, however, significant differences between the processes of acquiring either type of contract, with land contracts being easier to get.

A mortgage works like other types of loans. The lender lends the borrower money for a certain period, which they must repay with interest. Mortgages, however, are different because they are secured. Lenders obtain a hold over the property and can foreclose if the borrower fails to pay.

Mortgage loans can be used to buy or refinance any real estate or borrow against an existing property's value. The property provided serves as collateral for the loan. Lenders will assess the collateral provided to determine how much the borrower can borrow. But which is better?

Advantages and Disadvantages of Land Contracts

Land contracts, land purchase agreement forms, and contracts for deed or installment sales are agreements where the property owner agrees to relinquish ownership of the property once you complete your obligations. In most contracts, there is a monthly payment and a balloon payment at a later time.

Land contracts' specific advantages and disadvantages may vary depending on the contract terms and circumstances. Here are several advantages and disadvantages of land contracts:

Advantages of land contracts

- Credit: With land contracts, you can buy a property you might not otherwise qualify for with traditional financing if you have poor credit.

- Interest rate: Negotiating a lower interest rate with a land contract than a traditional mortgage is possible, potentially saving you money.

- Payment: A land contract may allow for smaller, more frequent payments or the opportunity to pay off the contract early without penalty.

- Ownership: A land contract gives the buyer immediate ownership of the property. The seller can use a quitclaim deed to show the buyer's interest in the property, especially if it's family.

Disadvantages of land contracts

- Credit: Even if a poor credit score does not prevent you from entering into land contracts, it may result in higher interest rates.

- Interest rate: You may pay a higher interest rate with land contracts since they are not regulated like traditional mortgages.

- Payment: Payments on land contracts are often higher and shorter than those on traditional mortgages, making them difficult for some buyers to afford.

- Ownership: Sellers retain ownership of the property until the buyer pays off the full amount of the land contract, so if the buyer falls behind on payments, they may lose it.

Advantages and Disadvantages of Mortgages

A mortgage is a type of loan that helps buyers raise immediate funds to purchase real estate, using the property as collateral. Borrowers repay the loan in installments over a set period, which can span years or decades.

This structure makes it easier for individuals to afford high property prices without paying upfront.

Mortgages are often referred to as a "claim on a property" or a "lien on a property," emphasizing the lender's security interest in the property until the loan is fully repaid.

Eligibility for a mortgage depends heavily on financial factors such as income, credit score, down payment amount, and the type of property being purchased.

Depending on the individual loan's terms and the borrower's circumstances, mortgages have varying advantages and disadvantages. Before accepting a mortgage, anyone considering one should carefully review and understand the terms of the loan.

Mortgages have some potential advantages, including:

- Credit: Most lenders offer mortgages to borrowers with a higher credit score, and a higher score may result in a lower rate.

- Interest rate: Because the collateral for the loan is the purchased property, mortgages typically carry lower interest rates than other types of loans.

- Payment: The length of mortgage terms can result in lower monthly payments and make home ownership more affordable for many people.

- Ownership: The borrower can then sell or use the property as collateral for another loan after repaying the mortgage.

Disadvantages:

- Credit: With poor credit, you may have difficulty qualifying for a mortgage or only qualify for mortgage loans with a higher interest rate and fewer favorable terms.

- Interest rate: Despite mortgage interest rates being generally lower than other types of loans, some factors, such as credit score and down payment size, can cause them to be relatively high.

- Payment: Longer mortgage terms can reduce monthly payments and result in borrowers paying more interest over time. Further, a borrower who falls behind on payments risks losing their property to foreclosure.

- Ownership: Banks and lenders retain ownership of properties until the mortgage is fully repaid, and they may restrict how you use the property. If borrowers fail to make timely payments, lenders can foreclose on the property, seizing and selling it to recover losses

- Additional costs: Borrowers who make a down payment of less than 20% may be required to pay for private mortgage insurance (PMI). This additional cost protects lenders against default but increases monthly expenses for borrowers.

Types of mortgages

When considering a mortgage, you should understand the different types available, as each comes with its own advantages and risks.

Below are the most common types of mortgages.

Fixed-rate mortgages

These loans have a set interest rate that remains constant throughout the repayment period.

This ensures predictable and consistent monthly payments, making them a popular choice for borrowers who value stability and long-term financial planning.

Adjustable-rate mortgages (ARMs)

ARMs begin with a fixed interest rate for an initial period—often 5, 7, or 10 years—but then adjust periodically based on market conditions.

While ARMs typically offer lower initial payments compared to fixed-rate loans, they carry the risk of higher payments if interest rates rise after the initial period.

Other types of mortgages

Some niche mortgage products, such as interest-only mortgages, allow borrowers to pay only the interest for a specified period before transitioning to higher payments that include principal.

These types of loans are less common due to their higher risk and were scrutinized heavily following past housing market crises.

Understanding these mortgage types can help you choose the best option for your financial situation and long-term goals.

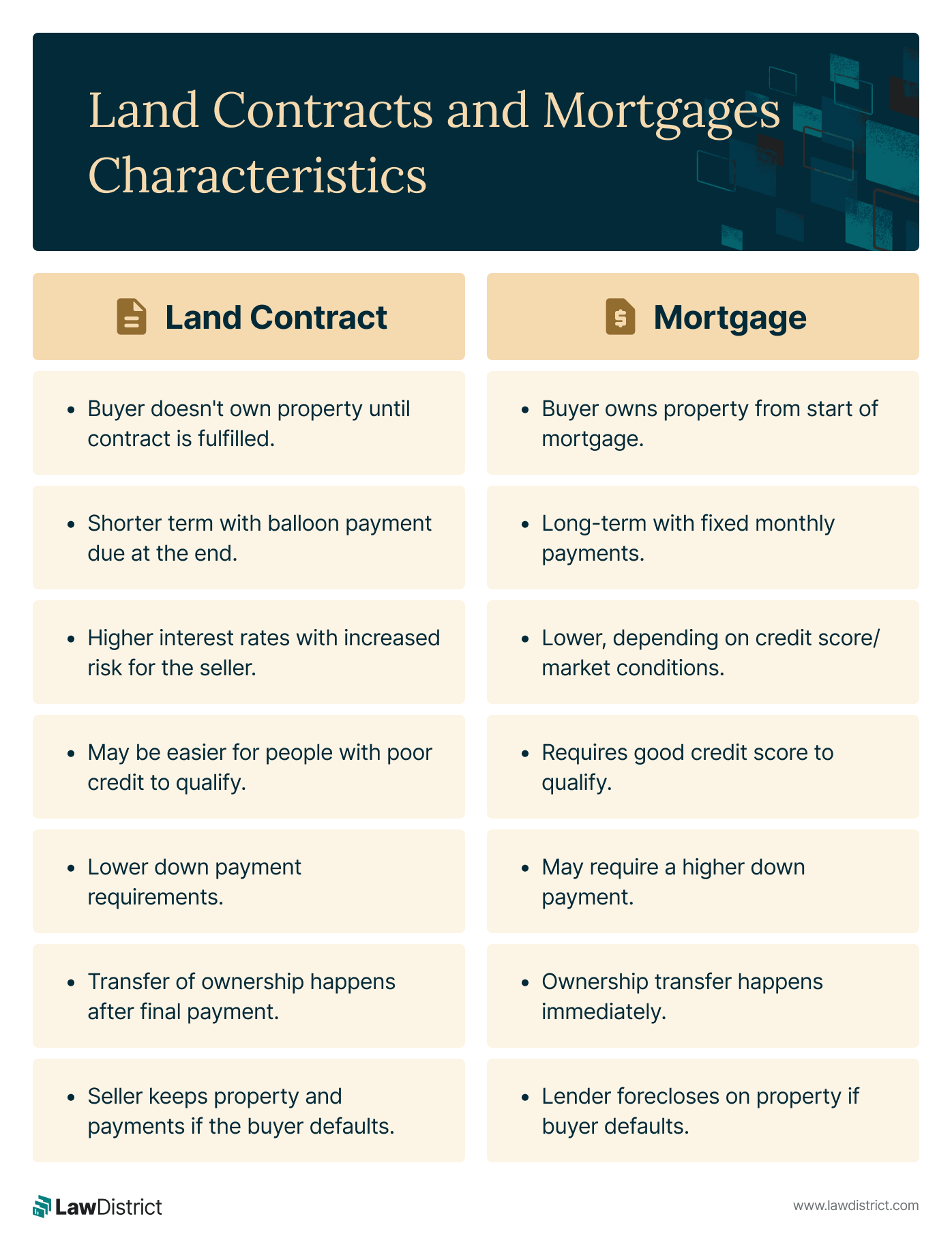

Difference Between Land Contracts and Mortgages

Now that we’ve outlined the advantages and disadvantages of each type, the following table will outline the major differences between these two types of agreements.

Examples of Land Contracts and Mortgages

A land contract and a mortgage are legal instruments used in real estate transactions, but each has its applications and benefits. Here are examples of when to use each option:

Land contract examples:

- If the buyer has poor credit, it may be challenging to obtain a traditional mortgage. But, considering that the seller acts as the lender and may be more flexible with credit requirements, a land contract might be a viable option.

- A land contract may be a better option if the property has some issue that makes it difficult to get a traditional mortgage, like zoning violations or an absence of a certificate of occupancy.

- If the buyer can't afford a large down payment, unlike a traditional mortgage, a land contract can allow the buyer and seller to negotiate the down payment amount.

Mortgage examples:

- In the case of good credit, a buyer might get a traditional mortgage with a lower interest rate than what would be offered to them in a land contract.

- A traditional mortgage may be the best option if the property has a clear title, meaning there are no liens or other issues. In most cases, lenders require a clear title to protect their investment.

- If the buyer has a large down payment, they may qualify for a traditional mortgage with a lower interest rate. Because the lender will see the buyer as less likely to default, the lender will approve the loan.

Final Word: Choosing Between a Land Contract and a Mortgage

Choosing between a land contract and a mortgage depends on your financial situation, goals, and the property’s specifics.

Use the following questions to guide your decision:

- Do I have good credit? Mortgages favor strong credit, while land contracts may work for lower scores.

- Can I afford a large down payment? Mortgages often require 10–20%, but land contracts may be more flexible.

- Am I prepared for long-term payments? Mortgages are long-term, while land contracts may involve shorter terms or balloon payments.

- Is the property title clear? Ensure there are no title issues with a land contract.

- What are my plans for the property? Consider whether your use is short- or long-term.

- Can I handle additional costs? Mortgages may include PMI, while land contracts might have higher interest rates.

Answering these questions can help you make the best choice for your financial and homeownership goals. Take the time to weigh all the pros and cons with our professional land contract guide.

Start Your Land Purchase Agreement Form Now

Helpful Resources:

Key Takeaways

- Land contracts offer flexible financing for buyers with poor credit but come with higher risks, such as balloon payments and less protection.

- Mortgages provide stability with predictable terms but require good credit and a down payment, and they may include costs like PMI.

- Key differences include ownership transfer (immediate with mortgages, delayed in land contracts) and regulatory oversight.

- Choosing the right option depends on credit, finances, and long-term goals.

Many similarities exist between a land contract and a mortgage. Both require monthly principal and interest payments, as well as a down payment. There are, however, significant differences between the processes of acquiring either type of contract, with land contracts being easier to get.

A mortgage works like other types of loans. The lender lends the borrower money for a certain period, which they must repay with interest. Mortgages, however, are different because they are secured. Lenders obtain a hold over the property and can foreclose if the borrower fails to pay.

Mortgage loans can be used to buy or refinance any real estate or borrow against an existing property's value. The property provided serves as collateral for the loan. Lenders will assess the collateral provided to determine how much the borrower can borrow. But which is better?

Advantages and Disadvantages of Land Contracts

Land contracts, land purchase agreement forms, and contracts for deed or installment sales are agreements where the property owner agrees to relinquish ownership of the property once you complete your obligations. In most contracts, there is a monthly payment and a balloon payment at a later time.

Land contracts' specific advantages and disadvantages may vary depending on the contract terms and circumstances. Here are several advantages and disadvantages of land contracts:

Advantages of land contracts

- Credit: With land contracts, you can buy a property you might not otherwise qualify for with traditional financing if you have poor credit.

- Interest rate: Negotiating a lower interest rate with a land contract than a traditional mortgage is possible, potentially saving you money.

- Payment: A land contract may allow for smaller, more frequent payments or the opportunity to pay off the contract early without penalty.

- Ownership: A land contract gives the buyer immediate ownership of the property. The seller can use a quitclaim deed to show the buyer's interest in the property, especially if it's family.

Disadvantages of land contracts

- Credit: Even if a poor credit score does not prevent you from entering into land contracts, it may result in higher interest rates.

- Interest rate: You may pay a higher interest rate with land contracts since they are not regulated like traditional mortgages.

- Payment: Payments on land contracts are often higher and shorter than those on traditional mortgages, making them difficult for some buyers to afford.

- Ownership: Sellers retain ownership of the property until the buyer pays off the full amount of the land contract, so if the buyer falls behind on payments, they may lose it.

Advantages and Disadvantages of Mortgages

A mortgage is a type of loan that helps buyers raise immediate funds to purchase real estate, using the property as collateral. Borrowers repay the loan in installments over a set period, which can span years or decades.

This structure makes it easier for individuals to afford high property prices without paying upfront.

Mortgages are often referred to as a "claim on a property" or a "lien on a property," emphasizing the lender's security interest in the property until the loan is fully repaid.

Eligibility for a mortgage depends heavily on financial factors such as income, credit score, down payment amount, and the type of property being purchased.

Depending on the individual loan's terms and the borrower's circumstances, mortgages have varying advantages and disadvantages. Before accepting a mortgage, anyone considering one should carefully review and understand the terms of the loan.

Mortgages have some potential advantages, including:

- Credit: Most lenders offer mortgages to borrowers with a higher credit score, and a higher score may result in a lower rate.

- Interest rate: Because the collateral for the loan is the purchased property, mortgages typically carry lower interest rates than other types of loans.

- Payment: The length of mortgage terms can result in lower monthly payments and make home ownership more affordable for many people.

- Ownership: The borrower can then sell or use the property as collateral for another loan after repaying the mortgage.

Disadvantages:

- Credit: With poor credit, you may have difficulty qualifying for a mortgage or only qualify for mortgage loans with a higher interest rate and fewer favorable terms.

- Interest rate: Despite mortgage interest rates being generally lower than other types of loans, some factors, such as credit score and down payment size, can cause them to be relatively high.

- Payment: Longer mortgage terms can reduce monthly payments and result in borrowers paying more interest over time. Further, a borrower who falls behind on payments risks losing their property to foreclosure.

- Ownership: Banks and lenders retain ownership of properties until the mortgage is fully repaid, and they may restrict how you use the property. If borrowers fail to make timely payments, lenders can foreclose on the property, seizing and selling it to recover losses

- Additional costs: Borrowers who make a down payment of less than 20% may be required to pay for private mortgage insurance (PMI). This additional cost protects lenders against default but increases monthly expenses for borrowers.

Types of mortgages

When considering a mortgage, you should understand the different types available, as each comes with its own advantages and risks.

Below are the most common types of mortgages.

Fixed-rate mortgages

These loans have a set interest rate that remains constant throughout the repayment period.

This ensures predictable and consistent monthly payments, making them a popular choice for borrowers who value stability and long-term financial planning.

Adjustable-rate mortgages (ARMs)

ARMs begin with a fixed interest rate for an initial period—often 5, 7, or 10 years—but then adjust periodically based on market conditions.

While ARMs typically offer lower initial payments compared to fixed-rate loans, they carry the risk of higher payments if interest rates rise after the initial period.

Other types of mortgages

Some niche mortgage products, such as interest-only mortgages, allow borrowers to pay only the interest for a specified period before transitioning to higher payments that include principal.

These types of loans are less common due to their higher risk and were scrutinized heavily following past housing market crises.

Understanding these mortgage types can help you choose the best option for your financial situation and long-term goals.

Difference Between Land Contracts and Mortgages

Now that we’ve outlined the advantages and disadvantages of each type, the following table will outline the major differences between these two types of agreements.

Examples of Land Contracts and Mortgages

A land contract and a mortgage are legal instruments used in real estate transactions, but each has its applications and benefits. Here are examples of when to use each option:

Land contract examples:

- If the buyer has poor credit, it may be challenging to obtain a traditional mortgage. But, considering that the seller acts as the lender and may be more flexible with credit requirements, a land contract might be a viable option.

- A land contract may be a better option if the property has some issue that makes it difficult to get a traditional mortgage, like zoning violations or an absence of a certificate of occupancy.

- If the buyer can't afford a large down payment, unlike a traditional mortgage, a land contract can allow the buyer and seller to negotiate the down payment amount.

Mortgage examples:

- In the case of good credit, a buyer might get a traditional mortgage with a lower interest rate than what would be offered to them in a land contract.

- A traditional mortgage may be the best option if the property has a clear title, meaning there are no liens or other issues. In most cases, lenders require a clear title to protect their investment.

- If the buyer has a large down payment, they may qualify for a traditional mortgage with a lower interest rate. Because the lender will see the buyer as less likely to default, the lender will approve the loan.

Final Word: Choosing Between a Land Contract and a Mortgage

Choosing between a land contract and a mortgage depends on your financial situation, goals, and the property’s specifics.

Use the following questions to guide your decision:

- Do I have good credit? Mortgages favor strong credit, while land contracts may work for lower scores.

- Can I afford a large down payment? Mortgages often require 10–20%, but land contracts may be more flexible.

- Am I prepared for long-term payments? Mortgages are long-term, while land contracts may involve shorter terms or balloon payments.

- Is the property title clear? Ensure there are no title issues with a land contract.

- What are my plans for the property? Consider whether your use is short- or long-term.

- Can I handle additional costs? Mortgages may include PMI, while land contracts might have higher interest rates.

Answering these questions can help you make the best choice for your financial and homeownership goals. Take the time to weigh all the pros and cons with our professional land contract guide.

Start Your Land Purchase Agreement Form Now

Helpful Resources:

Most Popular Posts

Some states require a motor vehicle bill of sale form; others do not. Even if only for your personal records, anyone who buys or sells a vehicle needs

If you plan to travel with a minor, whether or not you are their parent, you can minimize inconveniences by carrying a few necessary documents...