Foreclosure

What Is Foreclosure?

Foreclosure is the process a lender takes to recover money owed on a defaulted mortgage or contract for deed by taking ownership of the property. The steps can vary from state to state, but the process typically begins after a borrower misses a set number of monthly payments or fails to meet other terms in the loan agreement.

Most lenders try to avoid foreclosure by allowing borrowers time to get caught up with payments. The actual seizing of the property is often the final step after a lengthy process. In the U.S., the average foreclosure period was more than 900 days in 2022.

How Does Foreclosure Work?

The foreclosure process typically begins when a borrower is late on one or more mortgage payments. The lender sends a notice indicating that the month’s payment hasn’t been received.

If two payments are missed, the lender writes a demand letter to the borrower asking for immediate release of the missing payments. After 90 days of delinquent payments, the lender sends the borrower a notice of default.

The loan is then handed over to the lender’s foreclosure department, which notifies the borrower that they have 30 days to reinstate the loan by making the missed payments. The lender will continue the foreclosure process if the borrower does not handle missed payments during this reinstatement period.

How Does Foreclosure Affect the Borrower?

After a home is foreclosed upon, the occupants may receive a notice to quit letter or notice to vacate letter, which is another written warning that specifies a period (usually between three and 30 days) before they must vacate the premises.

If the residents do not leave the property, they can be sued. This type of legal action could hurt a borrower’s ability to rent or buy property again.

Additionally, a foreclosure will appear on a homeowner’s credit report within 30 to 60 days of the first missed payment and remain there for seven years. After seven years, the foreclosure is dropped from the borrower’s credit report.

A foreclosure can have negative consequences for the lender as well. In some states, when the court approves a foreclosure, the local sheriff holds an auction for the sale of the property in an effort to get back what the bank is owed. In other states, the bank sells the property in order to recoup its financial losses.

However, foreclosed properties are listed on a bank’s website and are attractive to investors. The properties often sell at a discount over non-foreclosed properties.

Foreclosure by State Can Vary

The required notices of missed payments, options for bringing the loan current, and the timeline for selling the property can vary from state to state.

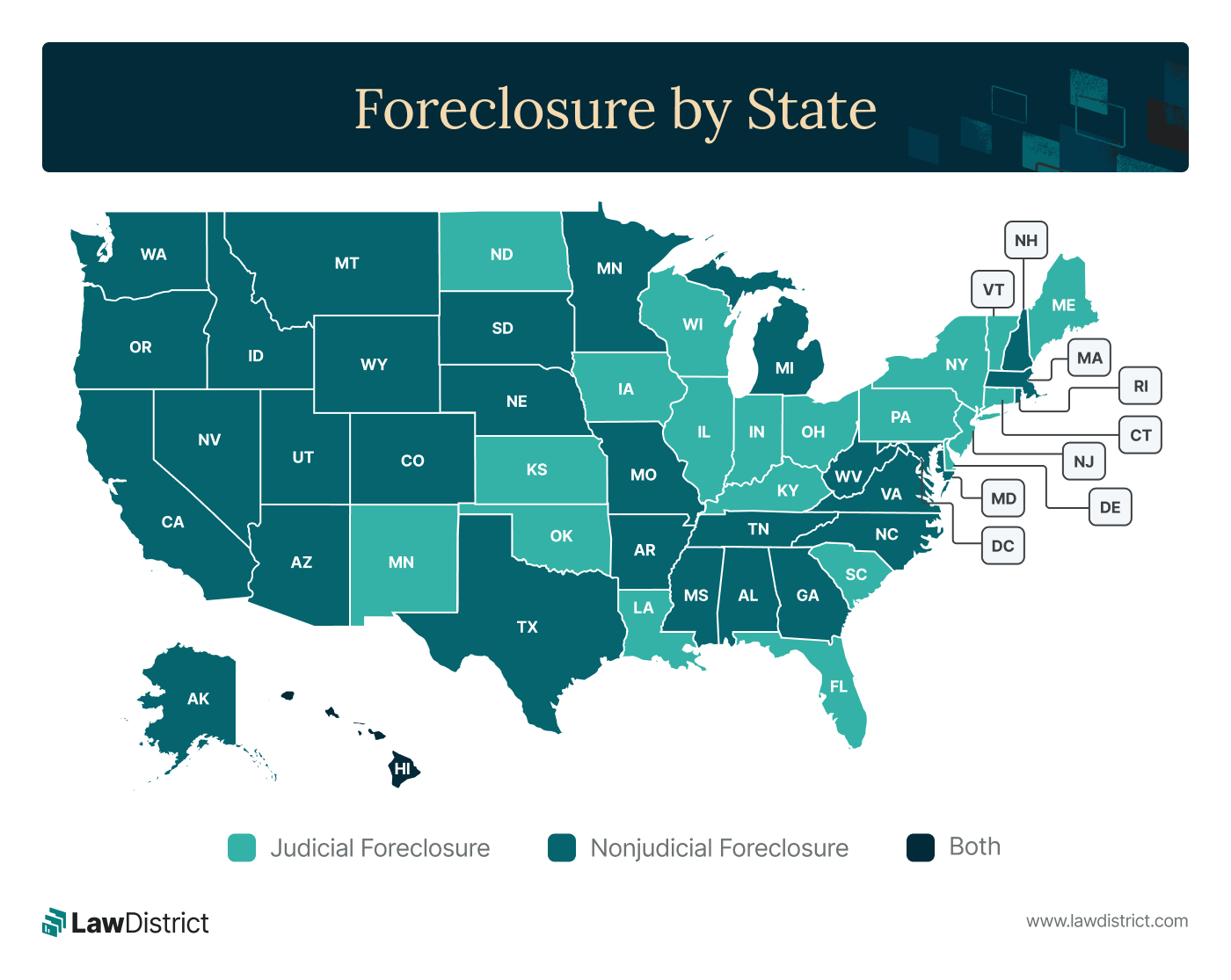

There are 22 states that use judicial foreclosure. In judicial foreclosure, the lender must request permission from the courts to foreclose on a home by proving the borrower has missed loan payments. The sheriff auctions the property to the highest bidder. This process can last several months to even years to complete.

On the other hand, 28 states use nonjudicial foreclosure (also called power of sale), which does not go through the court system. This process takes less time than a judicial foreclosure.

The District of Columbia and Hawaii use a combination of both methods, depending on the case.

Final Considerations

Understanding the difference between property deeds and titles is essential when dealing with a foreclosure. For example, a deed in lieu of foreclosure can be a way to avoid foreclosure. In this process, the property owner transfers the property title to the lender in exchange for a release from the debt.

Although the homeowner still must relinquish and vacate the property and relocate, they will avoid the foreclosure proceedings and its effect on their credit. In some cases, the lender might allow the borrower to lease the property back for a certain period of time.

Helpful Resources:

U.S. Department of Housing and Urban Development - Avoiding Foreclosure

What Is Foreclosure?

Foreclosure is the process a lender takes to recover money owed on a defaulted mortgage or contract for deed by taking ownership of the property. The steps can vary from state to state, but the process typically begins after a borrower misses a set number of monthly payments or fails to meet other terms in the loan agreement.

Most lenders try to avoid foreclosure by allowing borrowers time to get caught up with payments. The actual seizing of the property is often the final step after a lengthy process. In the U.S., the average foreclosure period was more than 900 days in 2022.

How Does Foreclosure Work?

The foreclosure process typically begins when a borrower is late on one or more mortgage payments. The lender sends a notice indicating that the month’s payment hasn’t been received.

If two payments are missed, the lender writes a demand letter to the borrower asking for immediate release of the missing payments. After 90 days of delinquent payments, the lender sends the borrower a notice of default.

The loan is then handed over to the lender’s foreclosure department, which notifies the borrower that they have 30 days to reinstate the loan by making the missed payments. The lender will continue the foreclosure process if the borrower does not handle missed payments during this reinstatement period.

How Does Foreclosure Affect the Borrower?

After a home is foreclosed upon, the occupants may receive a notice to quit letter or notice to vacate letter, which is another written warning that specifies a period (usually between three and 30 days) before they must vacate the premises.

If the residents do not leave the property, they can be sued. This type of legal action could hurt a borrower’s ability to rent or buy property again.

Additionally, a foreclosure will appear on a homeowner’s credit report within 30 to 60 days of the first missed payment and remain there for seven years. After seven years, the foreclosure is dropped from the borrower’s credit report.

A foreclosure can have negative consequences for the lender as well. In some states, when the court approves a foreclosure, the local sheriff holds an auction for the sale of the property in an effort to get back what the bank is owed. In other states, the bank sells the property in order to recoup its financial losses.

However, foreclosed properties are listed on a bank’s website and are attractive to investors. The properties often sell at a discount over non-foreclosed properties.

Foreclosure by State Can Vary

The required notices of missed payments, options for bringing the loan current, and the timeline for selling the property can vary from state to state.

There are 22 states that use judicial foreclosure. In judicial foreclosure, the lender must request permission from the courts to foreclose on a home by proving the borrower has missed loan payments. The sheriff auctions the property to the highest bidder. This process can last several months to even years to complete.

On the other hand, 28 states use nonjudicial foreclosure (also called power of sale), which does not go through the court system. This process takes less time than a judicial foreclosure.

The District of Columbia and Hawaii use a combination of both methods, depending on the case.

Final Considerations

Understanding the difference between property deeds and titles is essential when dealing with a foreclosure. For example, a deed in lieu of foreclosure can be a way to avoid foreclosure. In this process, the property owner transfers the property title to the lender in exchange for a release from the debt.

Although the homeowner still must relinquish and vacate the property and relocate, they will avoid the foreclosure proceedings and its effect on their credit. In some cases, the lender might allow the borrower to lease the property back for a certain period of time.

Helpful Resources:

U.S. Department of Housing and Urban Development - Avoiding Foreclosure