ACH Number

What Is an ACH Number?

An ACH (Automated Clearing House) number is a routing number used for electronic transactions between banks and other financial institutions. This number system was created in the 1970s when the shift to larger toward electronic banking began.

ACH numbers are used for electronic funds, transfers of small one-time payments, or scheduled recurring payments. ACH transactions include payroll and other direct deposits, consumer bills, tax refunds, tax payments, and other payment services.

An ACH number helps transfer the funds more quickly –often on the same day or the next business day– than paper check payments or transfers. ACH payments are often free, which makes a good way for businesses to pay salaries.

How Does an ACH Routing Number Work

An ACH routing number functions as a key component in processing electronic payments through the Automated Clearing House network. Without it, electronic transfers like direct deposits or bill payments would not be possible.

The first 2 digits of an ACH routing number indicate the Federal Reserve region where the institution is located, while the remaining numbers provide additional details about the specific bank.

This structure allows the ACH system to process millions of transactions daily with accuracy and efficiency.

When you initiate an ACH payment—such as setting up payroll deposits or paying a utility bill—the routing number works in combination with your account number. Together, they provide all the information needed to transfer funds securely between accounts.

This system is widely used because it offers a reliable and cost-effective way to handle electronic payments, often completing transactions within 1 business day.

ACH Numbers Vs. ABA Numbers

ABA (American Bankers Association) Numbers were developed in 1910 to help identify banks and financial institutions. They are typically nine digits long, with the first two numbers ranging between 00 and 12.

ABA numbers apply to paper checks, so they are sometimes referred to as check routing numbers. Smaller banks have a single routing number, while multi-national banks may have several numbers. Customers use routing numbers to pay bills, reorder checks, or set up a direct deposit account with an employer.

How to Find My ACH Routing Number

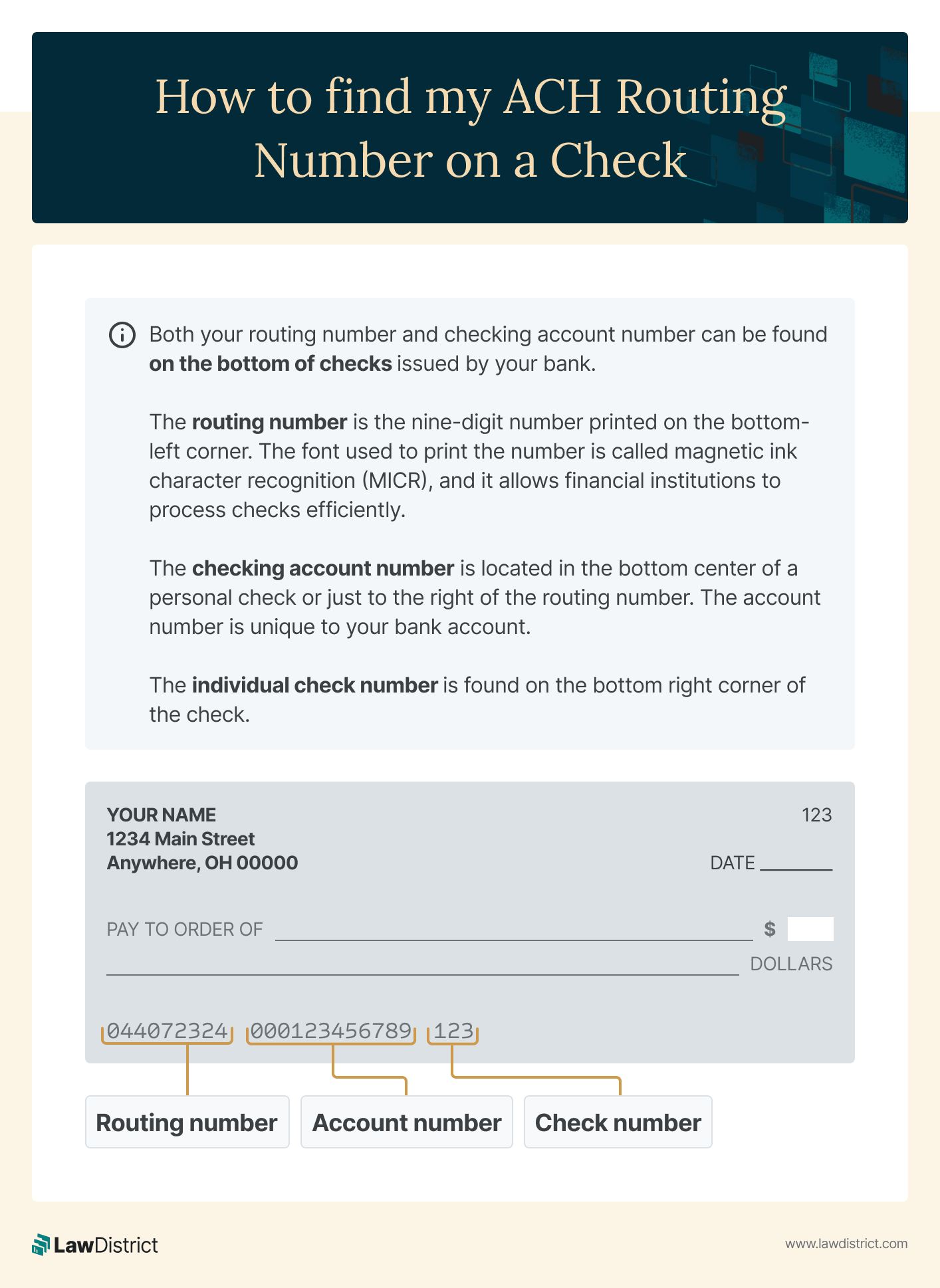

Both your routing number and checking account number can be found on the bottom of checks issued by your bank.

The routing number is the nine-digit number printed on the bottom-left corner. The font used to print the number is called magnetic ink character recognition (MICR), and it allows financial institutions to process checks efficiently.

The checking account number is located in the bottom center of a personal check or just to the right of the routing number. The account number is unique to your bank account.

The individual check number is found on the bottom right corner of the check.

If you don’t have a check, you can find your bank’s ACH and ABA routing numbers by visiting your bank’s website or a branch office. One bank can have many routing numbers, so your routing number will correspond to the bank location where you opened your account.

What Is an ACH Authorization Form?

An ACH authorization form is a document used to grant permission to a financial institution to debit or credit an individual or business account for the transfer of funds between bank accounts.

The form includes the following information:

- Account holder’s name and contact information

- Bank routing number

- Type of account (Checking or savings)

- Account number

- Specification of whether it is a debit or credit transaction

- Frequency of transactions

- Amount of each transaction

- Account holder’s signature

The ACH Network is managed by Nacha (formerly the National Automated Clearinghouse Association), an association for the electronic payments industry.

Start your ACH Authorization Form now

Helpful Resources:

Automated Clearing House - Home

Chase for Business - Know the difference between ABA and ACH routing numbers

What Is an ACH Number?

An ACH (Automated Clearing House) number is a routing number used for electronic transactions between banks and other financial institutions. This number system was created in the 1970s when the shift to larger toward electronic banking began.

ACH numbers are used for electronic funds, transfers of small one-time payments, or scheduled recurring payments. ACH transactions include payroll and other direct deposits, consumer bills, tax refunds, tax payments, and other payment services.

An ACH number helps transfer the funds more quickly –often on the same day or the next business day– than paper check payments or transfers. ACH payments are often free, which makes a good way for businesses to pay salaries.

How Does an ACH Routing Number Work

An ACH routing number functions as a key component in processing electronic payments through the Automated Clearing House network. Without it, electronic transfers like direct deposits or bill payments would not be possible.

The first 2 digits of an ACH routing number indicate the Federal Reserve region where the institution is located, while the remaining numbers provide additional details about the specific bank.

This structure allows the ACH system to process millions of transactions daily with accuracy and efficiency.

When you initiate an ACH payment—such as setting up payroll deposits or paying a utility bill—the routing number works in combination with your account number. Together, they provide all the information needed to transfer funds securely between accounts.

This system is widely used because it offers a reliable and cost-effective way to handle electronic payments, often completing transactions within 1 business day.

ACH Numbers Vs. ABA Numbers

ABA (American Bankers Association) Numbers were developed in 1910 to help identify banks and financial institutions. They are typically nine digits long, with the first two numbers ranging between 00 and 12.

ABA numbers apply to paper checks, so they are sometimes referred to as check routing numbers. Smaller banks have a single routing number, while multi-national banks may have several numbers. Customers use routing numbers to pay bills, reorder checks, or set up a direct deposit account with an employer.

How to Find My ACH Routing Number

Both your routing number and checking account number can be found on the bottom of checks issued by your bank.

The routing number is the nine-digit number printed on the bottom-left corner. The font used to print the number is called magnetic ink character recognition (MICR), and it allows financial institutions to process checks efficiently.

The checking account number is located in the bottom center of a personal check or just to the right of the routing number. The account number is unique to your bank account.

The individual check number is found on the bottom right corner of the check.

If you don’t have a check, you can find your bank’s ACH and ABA routing numbers by visiting your bank’s website or a branch office. One bank can have many routing numbers, so your routing number will correspond to the bank location where you opened your account.

What Is an ACH Authorization Form?

An ACH authorization form is a document used to grant permission to a financial institution to debit or credit an individual or business account for the transfer of funds between bank accounts.

The form includes the following information:

- Account holder’s name and contact information

- Bank routing number

- Type of account (Checking or savings)

- Account number

- Specification of whether it is a debit or credit transaction

- Frequency of transactions

- Amount of each transaction

- Account holder’s signature

The ACH Network is managed by Nacha (formerly the National Automated Clearinghouse Association), an association for the electronic payments industry.

Start your ACH Authorization Form now

Helpful Resources:

Automated Clearing House - Home

Chase for Business - Know the difference between ABA and ACH routing numbers