Amortization Schedule

What Is an Amortization Schedule?

An amortization schedule is a table that shows you how long it will take to pay off your mortgage over time through monthly payments. This schedule follows the payment agreement plan –typically a 15- or 30-year term– that you have worked out with your lender.

When a borrower takes out a loan to pay for a home, car, or other purchases, they typically make a payment at the same time each month. Part of the payment covers the interest due on the loan, and the rest goes toward reducing the principal loan amount.

An amortization schedule (also called an amortization table) shows how this process works over time and what the lender owes on any given month if they follow the plan.

What You Need to Know About an Amortization Schedule

The amortization schedule is based on the following components of your home loan agreement:

- Principal. The principal is the amount of money you borrow from your lender to buy the home. As you pay back the loan, the principal balance goes down, and your equity in the home goes up.

- Interest. The interest is the fee the lender charges for lending you the money to buy the home. The amount is based on a percentage of the principal.

In most cases, the bank or lending institution provides the borrower with the amortization schedule at the time all parties sign the personal loan agreement. Usually, the lender provides the balance owed after each monthly payment, so the borrower can see the total debt decreasing as they repay the loan. The document typically includes a summary of all interest payments throughout the loan period.

Start a Personal Loan Agreement now

Sometimes, the amortization schedule includes additional fees such as:

- origination fees

- closing costs

- early payment penalties

- property tax

- mortgage insurance

How Do You Calculate an Amortization Schedule?

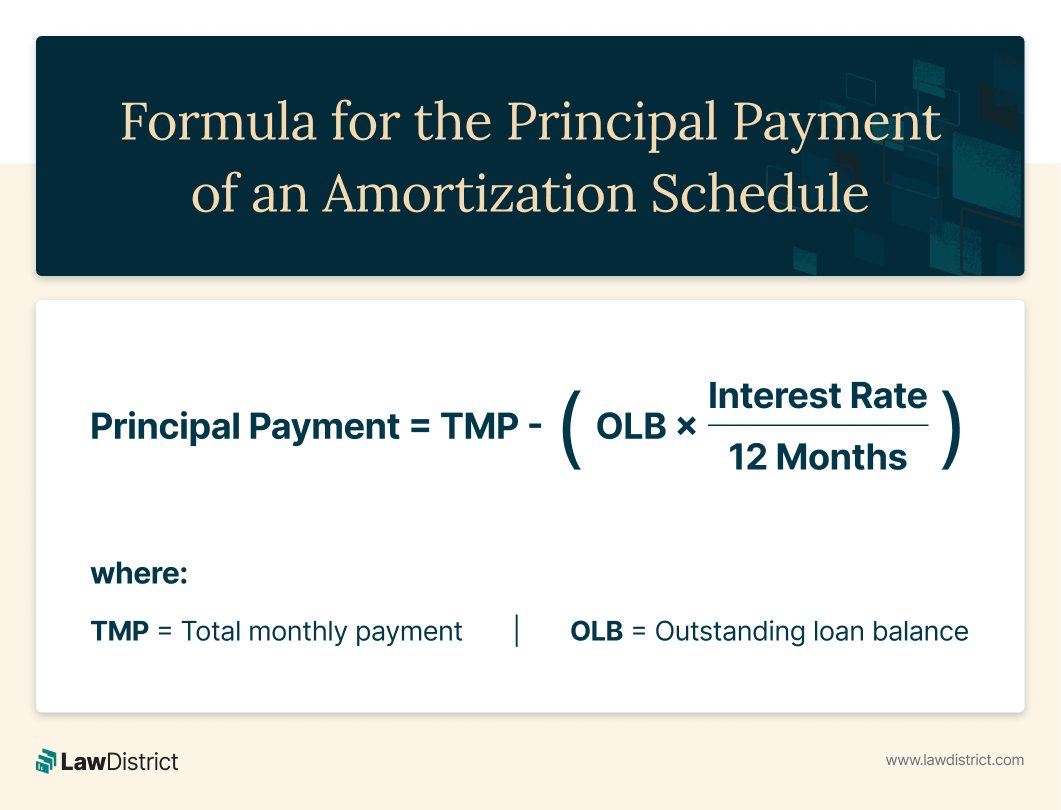

To figure out the principal payment of an amortization schedule, you must multiply your original principal balance by the interest rate. Then, divide that number by 12 months to determine your interest fee for the current month.

The final step is to subtract the interest fee from your total monthly payment. The number that remains is how much money will go toward your principal for that month. You repeat these steps each month until you have paid off your loan.

The following formula will help you calculate the principal payment of an amortization schedule:

Why Is an Amortization Schedule Important?

An amortization schedule is a visual reminder of how much interest you will pay over the lifetime of a home loan. It can serve as an incentive to make extra payments when you can since they will reduce the principal and thereby reduce the amount of interest you will pay.

As the principal decreases on the amortization schedule, the borrower’s equity in the home increases. A home equity loan –often called a second mortgage– allows you to cash out without needing a full refinance. A home equity loan can be used for home renovations or other purchases or purposes.

Understanding and following an amortization schedule can help make managing your finances easier.

Helpful Resources:

Assurance Financial - What Is a Loan Amortization Schedule?

Ramsey Solutions - What Is an Amortization Schedule and How Does It Work?

What Is an Amortization Schedule?

An amortization schedule is a table that shows you how long it will take to pay off your mortgage over time through monthly payments. This schedule follows the payment agreement plan –typically a 15- or 30-year term– that you have worked out with your lender.

When a borrower takes out a loan to pay for a home, car, or other purchases, they typically make a payment at the same time each month. Part of the payment covers the interest due on the loan, and the rest goes toward reducing the principal loan amount.

An amortization schedule (also called an amortization table) shows how this process works over time and what the lender owes on any given month if they follow the plan.

What You Need to Know About an Amortization Schedule

The amortization schedule is based on the following components of your home loan agreement:

- Principal. The principal is the amount of money you borrow from your lender to buy the home. As you pay back the loan, the principal balance goes down, and your equity in the home goes up.

- Interest. The interest is the fee the lender charges for lending you the money to buy the home. The amount is based on a percentage of the principal.

In most cases, the bank or lending institution provides the borrower with the amortization schedule at the time all parties sign the personal loan agreement. Usually, the lender provides the balance owed after each monthly payment, so the borrower can see the total debt decreasing as they repay the loan. The document typically includes a summary of all interest payments throughout the loan period.

Start a Personal Loan Agreement now

Sometimes, the amortization schedule includes additional fees such as:

- origination fees

- closing costs

- early payment penalties

- property tax

- mortgage insurance

How Do You Calculate an Amortization Schedule?

To figure out the principal payment of an amortization schedule, you must multiply your original principal balance by the interest rate. Then, divide that number by 12 months to determine your interest fee for the current month.

The final step is to subtract the interest fee from your total monthly payment. The number that remains is how much money will go toward your principal for that month. You repeat these steps each month until you have paid off your loan.

The following formula will help you calculate the principal payment of an amortization schedule:

Why Is an Amortization Schedule Important?

An amortization schedule is a visual reminder of how much interest you will pay over the lifetime of a home loan. It can serve as an incentive to make extra payments when you can since they will reduce the principal and thereby reduce the amount of interest you will pay.

As the principal decreases on the amortization schedule, the borrower’s equity in the home increases. A home equity loan –often called a second mortgage– allows you to cash out without needing a full refinance. A home equity loan can be used for home renovations or other purchases or purposes.

Understanding and following an amortization schedule can help make managing your finances easier.

Helpful Resources:

Assurance Financial - What Is a Loan Amortization Schedule?

Ramsey Solutions - What Is an Amortization Schedule and How Does It Work?