Free Personal Loan Agreement Template

Take advantage of our Personal Loan Agreement PDF template to safely lend money to another party. Download our pre-prepared document to set the terms of your loan in minutes.

Trusted by 4,859 users.

Protect your loan in minutes. What is the money for?

Fill forms in a few steps

Save, print & download

Done in 5 minutes

What Is a Personal Loan Agreement?

A Personal Loan Agreement serves as the formal record of a loan transaction between two entities, whether an individual and a financial institution or between private parties. It meticulously details the arrangement's critical components.

These typically include the principal sum transferred, the applicable interest rate, the structured repayment plan, and any other terms considered important to the agreement.

Additionally, this document can be key in setting the criteria for lending money to associates or relatives.

The types of agreements include:

- Secured: Includes collateral

- Fixed-rate: Keeps the interest rate the same throughout the repayment

- Co-sign: Makes someone else liable if the borrower has poor credit

- Variable rate: Ties interest rate to a third party

- Unsecured: Does not require collateral

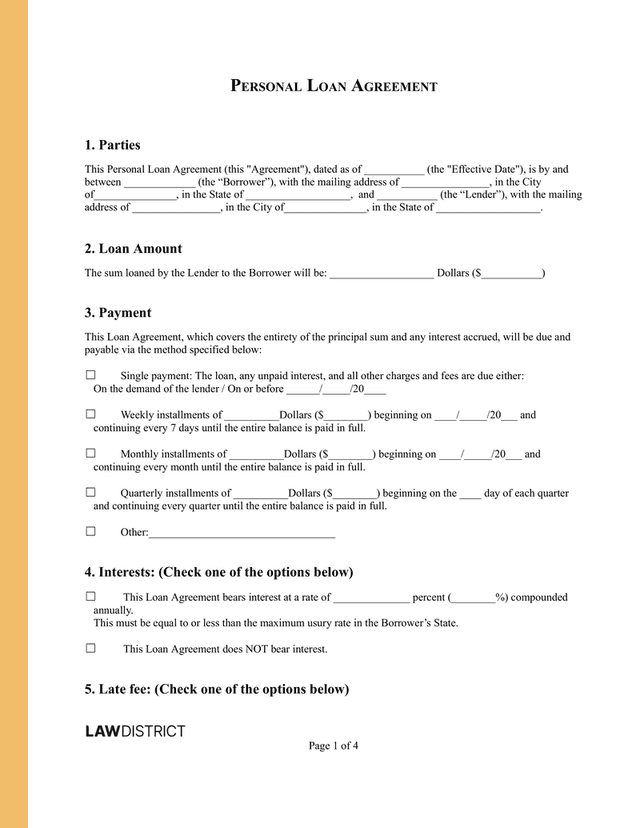

Personal Loan Agreement Sample

Understanding the structure and terms that you should use is key when creating your Loan Agreement.

To help you with that, we’ve included the following example.

When To Use a Personal Loan Agreement

Since most Personal Loans end up being unsecured, it’s a good idea to use them when lending money to friends or family members, as it helps to avoid misunderstandings and disputes.

This can be done to help cover the following types of costs:

- Funeral costs

- Family loans

- Medical costs

- Divorce costs

- Home repair

- Vehicle financing

- Debt consolidation

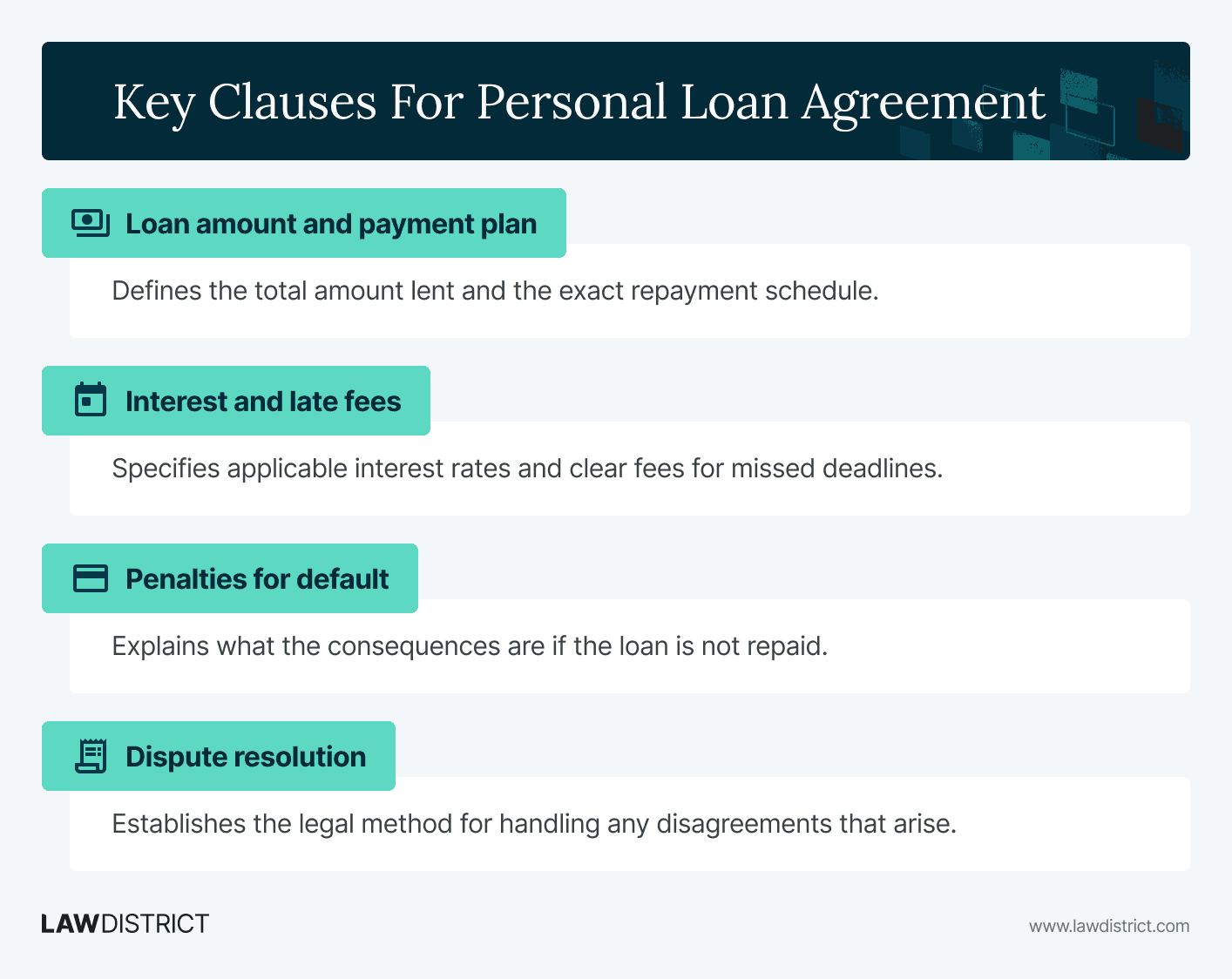

Key Clauses For Personal Loan Agreement

To make sure your loan is effective, it’s important to include the following clauses to make it clear how much is owed and when it must be paid.

How to Write a Personal Loan Agreement

Follow the steps below to create your Personal Loan Agreement.

- Include Parties: Identify both parties involved in the loan agreement by including full legal names, addresses, and contact information.

- State the amount: Include the amount of the loan.

- Provide payment options and interest: Specify how the loan will be repaid, for example, in one lump sum or in installments, the amount of interest, as well as any late fees.t.

- Mention the term: Mention when money will be disbursed and the repayment timeline.

- Add how income is verified: The methods of income verification are listed here.

- Define “Event of Acceleration”: State that if one event happens, the lender can declare the agreement immediately due and payable.

- Include a statement of remedies: Define the lender’s right to remedy any violation of the agreement.

- Mention a statement of subordination: Include a statement of the borrower’s obligation to repay the loan.

- Specify waivers: Declare that the lender cannot be deemed to have waived any rights provided by the agreement.

- State when legal expenses must be paid: Provide details on any attorney fees if the borrower agrees to pay legal fees.

- Include governing law: Include the law of the state this agreement will come into effect.

- Mention successors: Add written consent from the borrower’s successors to accept being bound to the loan.

- Leave space for signatures: Sign and date the agreement to indicate acceptance of the terms outlined in the document.

Make sure your document is correctly written by using our Personal Loan Agreement template to help write your document. Once you have your contract, you can have it reviewed by a legal professional.

Other Financial Templates

There are other documents that you can use in similar financial situations. Some of these related documents include:

FAQs About Personal Loan Agreements

Creating your document may lead to some confusion regarding signing requirements, terms, and more.

Review the responses to the most frequently asked questions on the subject to clear up your concerns.

A Personal Loan Agreement does not need to be notarized. However, when signing your document it is a good idea to do so in the presence of a notary public.

Even though it is not legally required, adding a notary’s signature adds validity to the document. This will further ensure that the agreement is enforceable in a court of law.

Before offering a family loan, consider alternatives like gifting the money without expecting repayment to prevent conflicts. You could also suggest they apply for a traditional personal loan, co-sign a loan to help them secure bank funding, or add them as an authorized user on your credit card.

Depending on your level of friendship and confidence with the other party in the agreement, you may want to create an unsecured personal loan agreement. However, the terms should still be listed clearly.

By clearly writing the terms and conditions you can avoid confusion and arguments down the line. If it’s a friend that you don’t completely trust you can also add collateral to the agreement.

A borrower can pay off a Personal Loan at any time before the due date. However, if a prepayment penalty is included in the agreement then they would also have to pay that fine.

By including a prepayment penalty the lender will be guaranteed to profit from making the loan. Otherwise, lenders lose out on interest if the borrower pays back the loan too early.

Try Lawdistrict Now

Instant and complete access to our entire library of legal forms

Edit, download and print in PDF from any device

Save time and money on legal document creation