Key Takeaways

- Estate planning ensures assets are distributed according to your wishes and reduces stress for loved ones.

- Key documents include a Last Will, Living Trust, Durable Power of Attorney, Healthcare Power of Attorney, and Living Will.

- Regular updates to your estate plan ensure it reflects changes in family, finances, or laws.

- Proper organization, such as secure storage and digital backups, is essential for accessibility and protection.

Estate planning is the process of organizing for the orderly transfer of properties after death. The ideal estate plan reduces taxes, expenses, and delays. Moreover, your assets reach the proposed beneficiaries.

An estate plan is a personalized plan tailored to your circumstances and situation. While professionals should handle some aspects of an estate plan, the person creating the plan can do most of the process.

Estate planning can be expensive, with attorney fees ranging from $1,000 to $3,000 or more for comprehensive plans. However, low-cost and DIY options are available for individuals with straightforward estates, offering a budget-friendly way to secure your assets and wishes.

Many believe estate plans are only for the wealthy or the elderly. But who defines "wealthy" and can tell when their time here is up? If you own property, you need an estate plan. In some cases, the process is straightforward, but in others, it can be complex and requires answering some basic questions:

- Who should receive your personal belongings and real property?

- Who do you want to be your children's guardian?

- Who should distribute your property?

- Will you leave part or all your estate to the charity of your choice?

- Do you want to disinherit anyone?

Estate planning allows your survivors to deal with their grief less stressfully. Below is a comprehensive estate planning checklist for the documents you might require to start the process.

Helpful Documents to Start Planning Your Estate

Before creating your estate plan, prepare detailed lists of your assets (e.g., financial accounts, real property, personal possessions), liabilities (e.g., mortgages, loans), heirs/beneficiaries, and digital accounts (e.g., email and cloud storage).

This ensures nothing is overlooked and simplifies the planning process.

An estate plan requires several documents, and you can use each document to specify your wishes after death or appoint an agent to represent you. To create a comprehensive estate plan, you'll need the following documents:

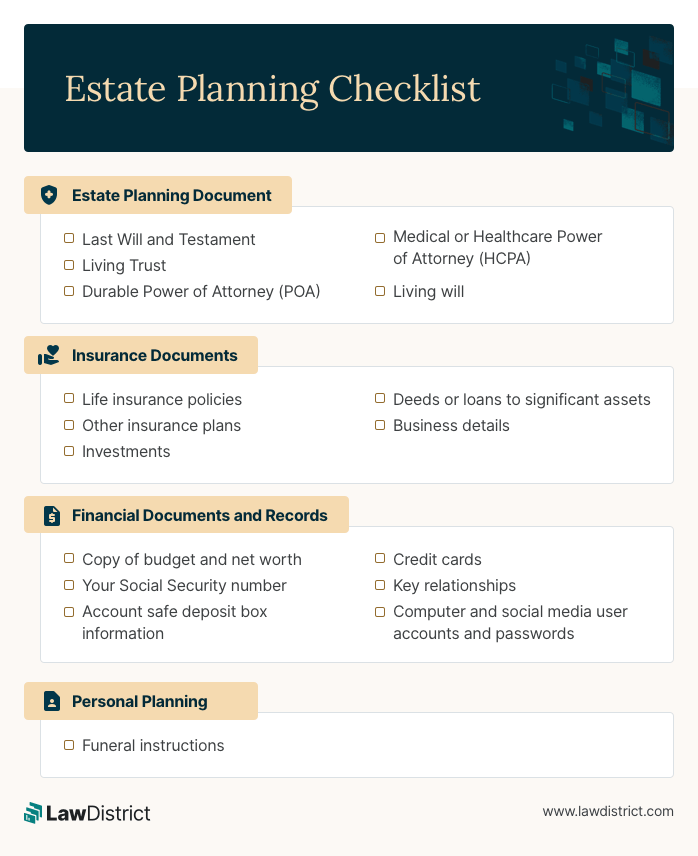

- Last Will and Testament

- Living Trust

- Durable Power of Attorney (POA)

- Medical or Healthcare Power of Attorney (HCPA)

- Living will

You may also want to include the following estate planning documents. The purpose of these documents is to help loved ones as well as streamline the estate closing process.

They include:

- Insurance policies details

- Financial and banking information

- Deeds and titles

- Digital logins and passwords

- Funeral instructions

As your family changes, you need to update your documents, so make sure to review them frequently. Below are five documents that can get you started on developing your estate plan.

Last Will and Testaments

A successful estate plan begins with your last will and testament. Your attorney will recommend a trust-based or a will-based estate plan once you start your estate planning journey. Will-based estate plans include:

- Your executor or personal representative settles your affairs and ensures all your wishes are followed.

- Your executor or personal representative's responsibilities and powers

- Your beneficiaries and what each will inherit

- Identifies a guardian for your minor children

Start Your Last Will and Testament Now

Living Trust

Often called a revocable living trust, this legal document allows you to transfer assets to beneficiaries and manage them during your lifetime. Creating a living trust does not require a threshold asset size. But families with large, complex estates and multiple beneficiaries often use it.

In case of death, your trustee transfers your assets to your beneficiaries as you wish. A revocable living trust helps avoid the lengthy probate process. But trusts involve maintenance, and if you fail to transfer important assets into your living trust, a pour-over will is valuable because it acts as a safety net for any assets you did not transfer before death.

Durable Power of Attorney (POA)

Durable powers of attorney grant someone the authority to act in a selection of legal and business matters and remain effective even when you are incapacitated. Sometimes named a durable power of attorney for finances.

POAs can take effect immediately or when you become incapacitated. Agents are also attorneys-in-fact, but they don't have to be lawyers. Transactions handled by an attorney-in-fact include:

- Selling and buying real property

- Bills, investments, and bank accounts management

- Remitting taxes

- Claiming government benefits

You may need a court to declare you incompetent without a general durable power of attorney. Having one in place is a good idea.

Start Your Durable Power of Attorney Now

Healthcare Power of Attorney (HCPA)

Healthcare Power of Attorney (HCPA) allows you to appoint someone else to handle your healthcare decisions. You appoint a person as your agent or healthcare proxy on the HCPA document.

A healthcare power of attorney is helpful if you can't express your wishes on medical care and treatment. The first-named HCPA can be replaced if unavailable and differ by state. So, consult your state's rules and forms when arranging one.

By coordinating with the patient's doctors, a healthcare proxy can avoid unnecessary treatments and make the right decisions for the patient.

Start Your Medical Power of Attorney Now

Living Will

Living wills can be helpful when faced with a life-threatening condition, and you can't communicate your treatment wishes. Resuscitation via electric shock, ventilation, and dialysis are all standard medical procedures a living will addresses. You can allow some of these procedures or none.

You can also specify whether to donate organs and tissues. Most states allow citizens to draft living wills; some call the document a medical advance directive or health care proxy. Depending on your state, you may make a detailed, tailored living will or be required to fill out a standardized form.

Insurance Documents

Unlike estate documents like wills, these documents are "contracts" you make with a company, and they are obligated to pay benefits to the named individuals. They include:

- Life insurance policies - Term life insurance and permanent life insurance

- Other insurance plans - Health and dental, homeowners or renters, and auto insurance

- Investments - Pension plans, annuities, bonds, mutual funds, and retirement accounts (IRAs, 401(k)s). Include all compensation plans in your disclosure and details about the transfer of accounts in your legacy plan.

- Deeds or loans to significant assets - Cars, homes, and boats.

- Business details - Buy-sell agreement, transition plans, key roles, etc.

Keep your beneficiary designations up-to-date and align them with your overall estate planning.

Financial Documents and Records

Experts recommend consulting a legal professional if you have a complex estate. A complicated estate plan may include multimillion-dollar estates, second marriages, blended families, and business ventures outside the United States. The documents to organize are:

- Budget and net worth copy - Identify assets, liabilities, income, and expenses.

- Your Social Security number - Includes how to claim benefits, how to collect, and where to claim.

- Account safe deposit box information - Keep records of all checking and savings accounts and the safe deposit keys.

- Credit cards - Latest credit report, including inactive ones.

- Key relationships - Contact information for your financial advisor, insurance agent, estate lawyer, accountant, executor, beneficiaries, and trustee.

- Computer and social media user accounts and passwords - Including social media and email accounts

- For example, memberships for professionals or individuals - Veterans' groups may offer death benefits.

Document Organization

Proper organization and secure storage of your estate planning documents are essential to ensure they are accessible when needed.

- Store your estate plan in a secure location, such as a safe deposit box or a home safe, to protect it from loss or damage.

- Create digital backups stored securely online or on external drives for added protection.

- Inform trusted individuals, such as family members or executors, about the location of these documents and how to access them.

This ensures your estate plan is easily retrievable and safeguarded against unforeseen circumstances.

Ready To Plan Your Estate?

A stranger could control your assets if you don't have a plan. The legal distribution fees, should you die intestate (meaning without a will) as Aretha Franklin or Prince did, will drastically reduce the value of your estate. Your heirs will not inherit your life's earnings but receive them from attorneys, accountants, appraisers, and others.

These documents should be easily accessible to your executor, spouse, partner, or trusted individual.

Pros and Cons of DIY Estate Planning

DIY estate planning can be a practical solution for individuals with simple estates, but it's important to weigh its advantages and disadvantages before proceeding.

- Pros:

- Cost-effective, saving on attorney fees.

- Flexible and convenient to complete at your own pace.

- Educational, helping you understand the legal intricacies of estate planning.

- Cons:

- Lack of legal advice may lead to errors or omissions.

- Complex estates may not be adequately addressed.

- State-specific requirements must be followed carefully to ensure validity.

Key Takeaways

- Estate planning ensures assets are distributed according to your wishes and reduces stress for loved ones.

- Key documents include a Last Will, Living Trust, Durable Power of Attorney, Healthcare Power of Attorney, and Living Will.

- Regular updates to your estate plan ensure it reflects changes in family, finances, or laws.

- Proper organization, such as secure storage and digital backups, is essential for accessibility and protection.

Estate planning is the process of organizing for the orderly transfer of properties after death. The ideal estate plan reduces taxes, expenses, and delays. Moreover, your assets reach the proposed beneficiaries.

An estate plan is a personalized plan tailored to your circumstances and situation. While professionals should handle some aspects of an estate plan, the person creating the plan can do most of the process.

Estate planning can be expensive, with attorney fees ranging from $1,000 to $3,000 or more for comprehensive plans. However, low-cost and DIY options are available for individuals with straightforward estates, offering a budget-friendly way to secure your assets and wishes.

Many believe estate plans are only for the wealthy or the elderly. But who defines "wealthy" and can tell when their time here is up? If you own property, you need an estate plan. In some cases, the process is straightforward, but in others, it can be complex and requires answering some basic questions:

- Who should receive your personal belongings and real property?

- Who do you want to be your children's guardian?

- Who should distribute your property?

- Will you leave part or all your estate to the charity of your choice?

- Do you want to disinherit anyone?

Estate planning allows your survivors to deal with their grief less stressfully. Below is a comprehensive estate planning checklist for the documents you might require to start the process.

Helpful Documents to Start Planning Your Estate

Before creating your estate plan, prepare detailed lists of your assets (e.g., financial accounts, real property, personal possessions), liabilities (e.g., mortgages, loans), heirs/beneficiaries, and digital accounts (e.g., email and cloud storage).

This ensures nothing is overlooked and simplifies the planning process.

An estate plan requires several documents, and you can use each document to specify your wishes after death or appoint an agent to represent you. To create a comprehensive estate plan, you'll need the following documents:

- Last Will and Testament

- Living Trust

- Durable Power of Attorney (POA)

- Medical or Healthcare Power of Attorney (HCPA)

- Living will

You may also want to include the following estate planning documents. The purpose of these documents is to help loved ones as well as streamline the estate closing process.

They include:

- Insurance policies details

- Financial and banking information

- Deeds and titles

- Digital logins and passwords

- Funeral instructions

As your family changes, you need to update your documents, so make sure to review them frequently. Below are five documents that can get you started on developing your estate plan.

Last Will and Testaments

A successful estate plan begins with your last will and testament. Your attorney will recommend a trust-based or a will-based estate plan once you start your estate planning journey. Will-based estate plans include:

- Your executor or personal representative settles your affairs and ensures all your wishes are followed.

- Your executor or personal representative's responsibilities and powers

- Your beneficiaries and what each will inherit

- Identifies a guardian for your minor children

Start Your Last Will and Testament Now

Living Trust

Often called a revocable living trust, this legal document allows you to transfer assets to beneficiaries and manage them during your lifetime. Creating a living trust does not require a threshold asset size. But families with large, complex estates and multiple beneficiaries often use it.

In case of death, your trustee transfers your assets to your beneficiaries as you wish. A revocable living trust helps avoid the lengthy probate process. But trusts involve maintenance, and if you fail to transfer important assets into your living trust, a pour-over will is valuable because it acts as a safety net for any assets you did not transfer before death.

Durable Power of Attorney (POA)

Durable powers of attorney grant someone the authority to act in a selection of legal and business matters and remain effective even when you are incapacitated. Sometimes named a durable power of attorney for finances.

POAs can take effect immediately or when you become incapacitated. Agents are also attorneys-in-fact, but they don't have to be lawyers. Transactions handled by an attorney-in-fact include:

- Selling and buying real property

- Bills, investments, and bank accounts management

- Remitting taxes

- Claiming government benefits

You may need a court to declare you incompetent without a general durable power of attorney. Having one in place is a good idea.

Start Your Durable Power of Attorney Now

Healthcare Power of Attorney (HCPA)

Healthcare Power of Attorney (HCPA) allows you to appoint someone else to handle your healthcare decisions. You appoint a person as your agent or healthcare proxy on the HCPA document.

A healthcare power of attorney is helpful if you can't express your wishes on medical care and treatment. The first-named HCPA can be replaced if unavailable and differ by state. So, consult your state's rules and forms when arranging one.

By coordinating with the patient's doctors, a healthcare proxy can avoid unnecessary treatments and make the right decisions for the patient.

Start Your Medical Power of Attorney Now

Living Will

Living wills can be helpful when faced with a life-threatening condition, and you can't communicate your treatment wishes. Resuscitation via electric shock, ventilation, and dialysis are all standard medical procedures a living will addresses. You can allow some of these procedures or none.

You can also specify whether to donate organs and tissues. Most states allow citizens to draft living wills; some call the document a medical advance directive or health care proxy. Depending on your state, you may make a detailed, tailored living will or be required to fill out a standardized form.

Insurance Documents

Unlike estate documents like wills, these documents are "contracts" you make with a company, and they are obligated to pay benefits to the named individuals. They include:

- Life insurance policies - Term life insurance and permanent life insurance

- Other insurance plans - Health and dental, homeowners or renters, and auto insurance

- Investments - Pension plans, annuities, bonds, mutual funds, and retirement accounts (IRAs, 401(k)s). Include all compensation plans in your disclosure and details about the transfer of accounts in your legacy plan.

- Deeds or loans to significant assets - Cars, homes, and boats.

- Business details - Buy-sell agreement, transition plans, key roles, etc.

Keep your beneficiary designations up-to-date and align them with your overall estate planning.

Financial Documents and Records

Experts recommend consulting a legal professional if you have a complex estate. A complicated estate plan may include multimillion-dollar estates, second marriages, blended families, and business ventures outside the United States. The documents to organize are:

- Budget and net worth copy - Identify assets, liabilities, income, and expenses.

- Your Social Security number - Includes how to claim benefits, how to collect, and where to claim.

- Account safe deposit box information - Keep records of all checking and savings accounts and the safe deposit keys.

- Credit cards - Latest credit report, including inactive ones.

- Key relationships - Contact information for your financial advisor, insurance agent, estate lawyer, accountant, executor, beneficiaries, and trustee.

- Computer and social media user accounts and passwords - Including social media and email accounts

- For example, memberships for professionals or individuals - Veterans' groups may offer death benefits.

Document Organization

Proper organization and secure storage of your estate planning documents are essential to ensure they are accessible when needed.

- Store your estate plan in a secure location, such as a safe deposit box or a home safe, to protect it from loss or damage.

- Create digital backups stored securely online or on external drives for added protection.

- Inform trusted individuals, such as family members or executors, about the location of these documents and how to access them.

This ensures your estate plan is easily retrievable and safeguarded against unforeseen circumstances.

Ready To Plan Your Estate?

A stranger could control your assets if you don't have a plan. The legal distribution fees, should you die intestate (meaning without a will) as Aretha Franklin or Prince did, will drastically reduce the value of your estate. Your heirs will not inherit your life's earnings but receive them from attorneys, accountants, appraisers, and others.

These documents should be easily accessible to your executor, spouse, partner, or trusted individual.

Pros and Cons of DIY Estate Planning

DIY estate planning can be a practical solution for individuals with simple estates, but it's important to weigh its advantages and disadvantages before proceeding.

- Pros:

- Cost-effective, saving on attorney fees.

- Flexible and convenient to complete at your own pace.

- Educational, helping you understand the legal intricacies of estate planning.

- Cons:

- Lack of legal advice may lead to errors or omissions.

- Complex estates may not be adequately addressed.

- State-specific requirements must be followed carefully to ensure validity.

Most Popular Posts

Some states require a motor vehicle bill of sale form; others do not. Even if only for your personal records, anyone who buys or sells a vehicle needs

If you plan to travel with a minor, whether or not you are their parent, you can minimize inconveniences by carrying a few necessary documents...